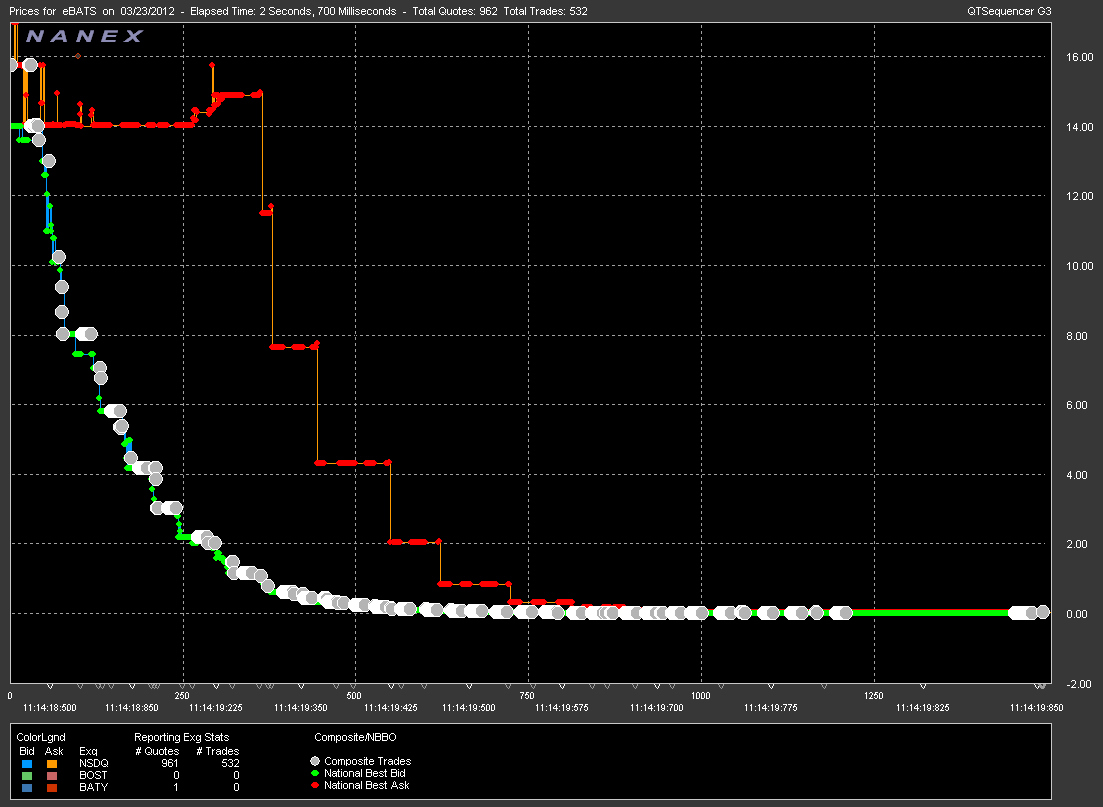

Stock Market Flaws Not So Rare, Data Shows

Stock market disruptions like the ones last week that temporarily shut down part of the nation’s third-largest exchange and briefly halted the trading of Apple shares are more common than investors may think.Although traders and the public were stunned by the problems on the BATS Global Markets stock exchange on Friday, a review of industry data shows that market disruptions large and small are a daily occurrence. The frequency of the problems has rattled the confidence of some investors and companies raising money through supercharged electronic markets.

The communication breakdown that blocked trading on parts of the BATS exchange for more than an hour has been seen in at least 110 instances across the nation’s 13 stock exchanges over the last year, a review of data from Nasdaq shows. That number has gone up every year since 2007.

In one instance in January, BATS said it was unable to trade with the New York Stock Exchange for nearly 30 minutes.

Meanwhile, exchanges have halted trading in company shares after sudden spikes or falls, as happened Friday with Apple, at least 265 times over the last year — more than one for every day of trading, according to data analyzed by the Tabb Group, a market research firm. These circuit breakers kick in after stocks experience 10 percent swings in a short period of time and can be caused by a technical error or waves of electronic trading on news developments. (...)

In addition, minor events at one exchange risk spiraling out through other exchanges and setting off a severe flash crash, like the one seen in May 6, 2010, when major markets fell more than 8 percent in a matter of minutes.

Blame for the market disturbances has fallen on the growing complexity and speed of the nation’s 13 official stock exchanges — three of which are owned by the New York Stock Exchange — and dozens of less official platforms for trading. A decade ago there were only two major trading platforms, and transaction times were measured in seconds.

A regulatory change in 2007 threw open the floodgates of competition by forcing stock trades to be routed to the exchange with the best price, as long as the exchange could act immediately. The proliferation of exchanges since then has lowered the price of trading for investors, and trade times are now measured in milliseconds. In the race for speed, however, some industry experts say reliability has been sacrificed. (...)

The S.E.C. and other regulators have been examining the vulnerabilities of the market, and the impact of high-speed trading, since the flash crash in May 2010. A new committee for the Commodity Futures Trading Commission examining the issue was set to meet for the first time on Thursday.

The S.E.C. has already taken several steps to head off moments of market chaos, including the circuit-breaker measures for 10 percent swings.

The circuit breakers have also provided a new window into how often such extreme market moves happen. During periods of calm trading, like January of this year, circuit breakers were used infrequently: 14 times, according to data analyzed by Tabb. In contrast, they were used 51 times in December. The figures do not indicate how often the problems were because of the exchanges rather than other factors.

Christopher Nagy, the head of order routing at the retail broker TD Ameritrade, compared circuit breakers to brakes on a car. They are important, he said, but they become less effective as the car goes faster, as the market has in recent years.

“When you see any sort of market strife, you see chaos erupt,” he said.

The S.E.C. is considering introducing other measures to monitor the markets, like a new system, known as limit up-limit down, to halt extreme trades before they can be executed. But some market watchers say the agency has not been able to keep up with the increasing speed and complexity of the markets.

“We’ve managed over the past few years to equip the traders with Ferraris,” said Richard Bentley, the vice president for capital markets at Progress Software, which provides the industry with technology, “and the regulators are trying to keep up with them on bicycles.”