In prima pagina il Sole 24 Ore oggi ospita un ariticolo di Nassim Taleb intitolato Dieci regole esclusive per stregare il cigno nero. L'ho letto sull'aereo che mi riportava a casa dalle vacanze (purtroppo finite) e mi chiedo se la redazione del giornale abbia fatto attenzione a quello che scrive Taleb oppure se siano stati un po' distratti, contando sul prolungarsi del balletto degli equivoci che permette a banchieri e gestori distratti e/o poco coscienziosi di invocare cigni neri ogniqualvolta le cose vanno (prevedibilmente, per chi non smette di ragionare) male. Ecco qualcuna delle 10 regole di Taleb

2. No alla socializzazione delle perdite e alla privatizzazione dei guadagni

Qualunque cosa possa aver bisogno di essere salvata da un dissesto dovrebbe essere nazionalizzata; qualsiasi cosa non abbia bisogno di essere salvata da un fallimento dev'essere libera, piccola e in grado di affrontare rischi. Noi siamo entrati nelle manifestazioni peggiori del capitalismo e del socialismo. In Francia, negli anni 80 del Novecento, i socialisti hanno assunto il controllo delle banche. Negli Stati Uniti, nel decennio 2001-2010 le banche hanno assunto il controllo del governo. Questa è una cosa surreale.

3. A coloro che hanno guidato uno scuolabus a occhi bendati (e lo hanno distrutto) non si dovrebbe mai affidare un altro autobus

L'establishment economico (le università, i regolamentatori, le banche centrali, i funzionari governativi, varie organizzazioni dotate di un personale formato in gran parte da economisti) perse la sua legittimità in coincidenza con il fallimento del sistema nel 2008. Sarebbe irresponsabile e folle riporre la nostra fiducia nella loro capacità di guidarci fuori da questo disastro. E da irresponsabili anche ascoltare consigli dagli "esperti di rischi" e dagli istituti di scienze commerciali che sostengono ancora le loro misurazioni e che ci hanno ridotto sul lastrico (come il metodo di misurazione del rischio value-at-risk). Scovate le persone intelligenti che hanno le mani pulite.

4. Non lasciare che una persona che si assicura un bonus di incentivazione possa gestire una centrale nucleare, e nemmeno i tuoi rischi finanziari

È molto probabile che una tale persona sia incline a fare tagli sulla sicurezza per presentare questi risparmi come "profitti", sostenendo di essere "prudente".

I bonus non si conciliano con i rischi nascosti di gravi imprevisti. È stata l'asimmetria del sistema dei bonus a condurci alla situazione attuale. Non ci sono incentivi senza disincentivi: il capitalismo distribuisce premi e punizioni, non solo premi.

![[SCISSORS]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_u1e454bacouq4AZIl03HdHz9yVbGnzeVl3z5T2us_4l31F1BplxWlCiwS8jNSisTZxuSYEZGAHa8ijdj7SBfznVND1FhOZWL42os9iKYXrYBfH7H2V-rXCuVrT3Gst9Z4ivRBtWpxjcPNgcLnO_z4PCgQ=s0-d)

Questo ETF non è armonizzato e in Italia l'unico ETF short con leva doppia è BUND2S.MI che ha come indice di riferimento il Bund future (la cui galoppata continua da oltre quattro mesi e pare inarrestabile).

A favore della tesi di una bolla nelle obbligazioni governative si sono espressi Jeremy Siegel e Jeremy Schwartz sul Wall Street Journal di oggi:

secondo Siegel e Schwartz le valutazioni attuali delle obbligazioni non assicurano rendimenti ragionevoli in parte anche perchè we believe U.S. economic growth is likely to accelerate.

From our perspective, the safest bet for investors looking for income and inflation protection may not be bonds. Rather, stocks, particularly stocks paying high dividends, may offer investors a more attractive income and inflation protection than bonds over the coming decade.(...)

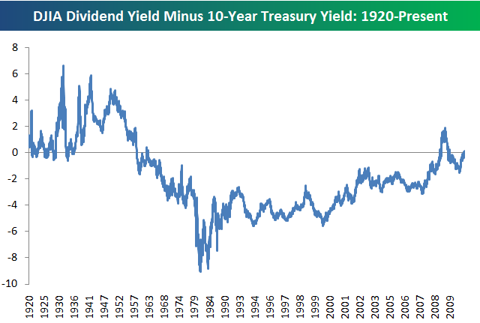

Today, the 10 largest dividend payers in the U.S. are AT&T, Exxon Mobil, Chevron, Procter & Gamble, Johnson & Johnson, Verizon Communications, Phillip Morris International, Pfizer, General Electric and Merck. They sport an average dividend yield of 4%, approximately three percentage points above the current yield on 10-year TIPS and over one percentage point ahead of the yield on standard 10-year Treasury bonds. Their average price-earnings ratio, based on 2010 estimated earnings, is 11.7, versus 13 for the S&P 500 Index. Furthermore, their earnings this year (a year that hardly could be considered booming economically) are projected to cover their dividend by more than 2 to 1.

Due to economic growth the dividends from stocks, in contrast with coupons from bonds, historically have increased more than the rate of inflation. The average dividend income from a portfolio of S&P 500 Index stocks grew at a rate of 5% per year since the index's inception in 1957, fully one percentage point ahead of inflation over the period. That growth rate includes the disastrous dividend reductions that occurred in 2009, the worst year for dividend cuts by far since the Great Depression.

Those who are now crowding into bonds and bond funds are courting disaster. The last time interest rates on Treasury bonds were as low as they are today was in 1955. The subsequent 10-year annual return to bonds was 1.9%, or just slightly above inflation, and the 30-year annual return was 4.6% per year, less than the rate of inflation.

Furthermore, the possibility of substantial capital losses on bonds looms large. If over the next year, 10-year interest rates, which are now 2.8%, rise to 3.15%, bondholders will suffer a capital loss equal to the current yield. If rates rise to 4% as they did last spring, the capital loss will be more than three times the current yield. Is there any doubt that interest rates will rise over the next two decades as the baby boomers retire and the enormous government entitlement programs kick into gear?

With future government finances so precarious, private asset accumulation and dividend income must become the major sources of retirement funding. At current interest rates, government bonds will not be the answer. One hundred times earnings was the tipping point for the tech market a decade ago. We believe that the same is now true for government bonds

Furthermore, economists generally agree that the most important determinant for long-term economic growth is productivity, not consumer demand. Despite the subpar productivity growth reported for the last quarter, the latest year-over-year productivity growth of 3.9% is almost twice the long-term average. For the first two quarters of this year productivity growth, at over 6%, was the highest since the 1960s.

Se condividete l'ottimismo sulle prospettive future dell'economia U.S.A. non potete esimervi dal condividere le conclusioni:

Today, the 10 largest dividend payers in the U.S. are AT&T, Exxon Mobil, Chevron, Procter & Gamble, Johnson & Johnson, Verizon Communications, Phillip Morris International, Pfizer, General Electric and Merck. They sport an average dividend yield of 4%, approximately three percentage points above the current yield on 10-year TIPS and over one percentage point ahead of the yield on standard 10-year Treasury bonds. Their average price-earnings ratio, based on 2010 estimated earnings, is 11.7, versus 13 for the S&P 500 Index. Furthermore, their earnings this year (a year that hardly could be considered booming economically) are projected to cover their dividend by more than 2 to 1.

Due to economic growth the dividends from stocks, in contrast with coupons from bonds, historically have increased more than the rate of inflation. The average dividend income from a portfolio of S&P 500 Index stocks grew at a rate of 5% per year since the index's inception in 1957, fully one percentage point ahead of inflation over the period. That growth rate includes the disastrous dividend reductions that occurred in 2009, the worst year for dividend cuts by far since the Great Depression.

Those who are now crowding into bonds and bond funds are courting disaster. The last time interest rates on Treasury bonds were as low as they are today was in 1955. The subsequent 10-year annual return to bonds was 1.9%, or just slightly above inflation, and the 30-year annual return was 4.6% per year, less than the rate of inflation.

Furthermore, the possibility of substantial capital losses on bonds looms large. If over the next year, 10-year interest rates, which are now 2.8%, rise to 3.15%, bondholders will suffer a capital loss equal to the current yield. If rates rise to 4% as they did last spring, the capital loss will be more than three times the current yield. Is there any doubt that interest rates will rise over the next two decades as the baby boomers retire and the enormous government entitlement programs kick into gear?

With future government finances so precarious, private asset accumulation and dividend income must become the major sources of retirement funding. At current interest rates, government bonds will not be the answer. One hundred times earnings was the tipping point for the tech market a decade ago. We believe that the same is now true for government bonds

Ma l'evidenza di una bolla nelle obbligazioni è così lampante secondo alcuni, che addirittura basta andare da McDonald per accorgersene! Non mi credete? Sentite qui: