Piccola rassegna di post sull'argomento obbligazioni e sull'Hindeburg Omen:

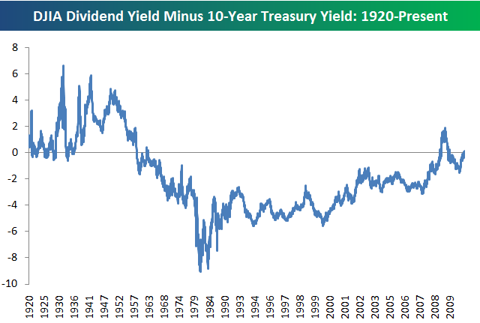

- iniziamo con due post di Bespoke: nel primo si contesta (senza un riferimento esplicito) l'affermazione che the Dow's dividend yield is now greater than the 10-Year Treasury yield (...and...) that this is the first time this has happened in decades, but in actuality, the Dow's yield got much higher than the 10-Year yield as recently as late 2008 and early 2009. La differenza oggi aumenta ancora con il calo del Dow e dello yield dei bond decennali dopo la pubblicazione dei dati economici U.S.A. così deludenti. Nel secondo, dedicato all'Hindenburg Omen, si fa osservare come

A closer look at the list of new highs, however, shows that the "stocks" hitting new highs last Thursday were hardly stocks at all. The WSJ provides a list of NYSE listed stocks hitting new highs and new lows on a daily basis, and looking at last Thursday's list of new highs shows that practically all of them were closed-end fixed income securities, preferred stocks, or some other form of fixed income product masquerading as an equity. In fact, of the 92 issues that hit new highs on Thursday (8/12), less than ten were common stocks.

Se si limita l'analisi del segnale alle azioni, escludendo quindi le obbligazioni scambiate sul NYSE e travestite da azioni, per esempio limitandosi ad analizzare le azioni che costituiscono l'indice S&P500 si scopre che il 12 agosto scorso only 0.2% of the stocks in the S&P 500 hit new highs while 5.6% of the stocks in the index hit new lows. A day when 5.6% of the stocks in the S&P 500 hit new lows is hardly a sign of strength, but it also doesn't reflect the indecision and confusion that the Hindenburg Omen is supposed to convey. Call us crazy, but an indicator that measures the internals of the equity market should probably avoid using fixed income securities in its analysis. On a side note, the Hindenburg Omen was last triggered in June 2008, and back then the indicator would have been triggered using either the NYSE or the S&P 500.

Insomma: non solo il fondamento statistico dell'Omen è perlomeno discutibile ma anche la sua definizione ha forse bisogno di qualche piccolo aggiustamento.

- Brad De Long contesta l'analisi dei monetaristi osservando come la velocità del denaro abbia oscillazioni sempre più ampie rispetto alla trendline e in questo post interviene nel dibattito sulla bolla nel mercato delle obbligazioni del Tesoro U.S.A., rispondendo all'articolo di Siegel e Schwartz sul WSJ e raccontato ieri da Alfaobeta. Secondo De Long in questo caso parlare di una bolla è fuorviante poichè A bubble--I thought--is when those holding an asset do so because they expect its price to rise more-or-less indefinitely, and such a price rise is impossible. Such a bubble is very prone to rapid collapse when people realize that their expectations are very wrong. Do holders of U.S. Treasury bonds expect the prices of the assets they own to rise more-or-less indefinitely? No, they do not. They expect their holdings of Treasury bonds to be and to continue to be safe places to park their money, and they expect other asset classes to be risky.

Over time, I think, the fear of other asset collapses will ebb--but this is highly likely to produce a gradual rise in the prices of other asset classes and a gradual fall in Treasury prices, but a gradual fall does not make Treasury bonds unsafe.

Those who hold Treasuries to maturity will get the returns they expect: for holders-to-maturity, Treasury bonds are indeed very safe absent a very unlikely upward leap in inflation.

So I cannot see any possibility of a bubble collapse at the short end of the Treasury market--less than ten years, seven.

Secondo De Long anche chi investe in obbligazioni con durata lunga, fino ai trenta anni, corre rischi molto limitati, specialmente se si tiene conto della situazione macroeconomica. La differenza di posizione con Siegel-Schwartz non è sorprendente perchè riflette anche visioni divergenti delle prospettive dell'economia U.S.A. come avevo osservato ieri nel commento al loro articolo. Ecco come conclude il suo post Brad De Long: Could there be a sudden large downward movement in Treasury bond prices that would convince holders of Treasuries that they are not safe at all and induce a wave of panicked selling that would look like the collapse of a bubble?

In asset prices, never say never: the only thing you can ever say with absolute certainty is J.P. Morgan's: "they will fluctuate."

But I don't think so. People today buy an on-the-run ten-year Treasury at a yield of 2.64%--the bond with a 2.65% coupon maturing on August 15, 2020 at a price of 100.07. Its price drops tomorrow to 88.96. Do they conclude that their long Treasury position is too risky to hold? Or do they conclude that the Treasury correction has come and gone, and that Treasuries are actually safer than ever?

To argue that there is a Treasury bond bubble going on, you have to believe that such a fall in Treasury bond prices would induce further selling. And I cannot see that--not with the current state of macroeconomic news.

Nessun commento:

Posta un commento