Buona parte della discussione sulla ristrutturazione o, meglio, sull rollover "volontario" del debito greco è influenzata dalla necessità di trovare una modalità sostenibile di spalmare l'enorme quantità di debito accumulato su più anni senza che questo significhi un'insolvenza conclamata che al di là dell'ignominia per l'eurozona di vedere un paese membro non ripagare i suoi debiti farebbe scattare i pagamenti sui credit default swaps. Cosa accadrebbe in questo caso è l'oggetto di un interessante articolo sul New York Times di qualche giorno fa che si interroga se la crisi del debito dei PIGS non possa nascondere un'altra A.I.G.: la risposta è tutt'altro che semplice vista la poca trasparenza del mondo dei derivati.

Buona parte della discussione sulla ristrutturazione o, meglio, sull rollover "volontario" del debito greco è influenzata dalla necessità di trovare una modalità sostenibile di spalmare l'enorme quantità di debito accumulato su più anni senza che questo significhi un'insolvenza conclamata che al di là dell'ignominia per l'eurozona di vedere un paese membro non ripagare i suoi debiti farebbe scattare i pagamenti sui credit default swaps. Cosa accadrebbe in questo caso è l'oggetto di un interessante articolo sul New York Times di qualche giorno fa che si interroga se la crisi del debito dei PIGS non possa nascondere un'altra A.I.G.: la risposta è tutt'altro che semplice vista la poca trasparenza del mondo dei derivati.But the possibility that some company out there may have insured billions of dollars of European debt has added a new tension to the sovereign default debate.

In years past, when financial crises in Argentina and Russia left those countries unable to make good on their government debts, they simply defaulted. But this time around, swaps and other sorts of contracts have become so common and so intertwined in the financial markets that there are fears among regulators and financial players about how a Greek default would play out among derivatives holders.

The looming uncertainties are whether these contracts — which insure against possibilities like a Greek default — are concentrated in the hands of a few companies, and if these companies will be able to pay out billions of dollars to cover losses during a default. If there were a single company standing behind many of these contracts, that company would be akin to the American International Group of the euro crisis. The American insurer needed a $182 billion federal bailout during the financial crisis because it had insured the performance of mortgage bonds through derivatives and could not pay on all of them.

Even regulators seem unsure of whether a Greek default would reveal such concentrated risk in the hands of just a few companies. Spokeswomen for the central banks of both Europe and the United States would not say whether their researchers had studied holdings of such contracts among nonbank entities like insurance companies and hedge funds.(...)

Derivatives traders and analysts are debating just how much money is involved in these contracts and what sort of threat they pose to markets in Europe and the United States. On the one hand, just over $5 billion is tied up in credit-default swap contracts that will pay out if Greece defaults, according to Markit, a financial data firm based in London. That is less than 1 percent the size of Greece’s economy, but that is a conservative calculation that counts protections banks have in place offsetting their positions, and is called the net exposure. The less conservative figure, the gross exposure, is $78.7 billion for Greece, according to Markit. And there are many other types of contracts, like about $44 billion in other guarantees tied to Greece, according to the Bank of International Settlements. The gross exposure of the five most financially pressed European Union countries — Portugal, Italy, Ireland, Greece and Spain — is about $616 billion. And the broader figure on all derivatives from those countries is unknown.

The pervasiveness of these opaque contracts has complicated negotiations for European officials, and it underscores calls for more transparency in the derivatives market.

The uncertainty, financial analysts say, has led European officials to push for a “voluntary” Greek bond financing solution that may sidestep a default, rather than the forced deals of other eras. “There’s not any clarity here because people don’t know,” said Christopher Whalen, editor of The Institutional Risk Analyst. “This is why the Europeans came up with this ridiculous deal, because they don’t know what’s out there. They are afraid of a default. The industry is still refusing to provide the disclosure needed to understand this. They’re holding us hostage. The Street doesn’t want you to see what they’ve written.”(...)

On Wall Street, traders are debating whether the industry’s process for unwinding credit-default swaps would run smoothly if Greece defaulted. The process is tightly controlled by a small group of bankers who meet in an industry group called the International Swaps and Derivatives Association.

The process is fairly well developed, but it has been little tested on the debt of countries. For the most part, Wall Street has cashed in on credit-default swaps tied to corporations’ debt.

For most purposes, determining whether a default occurred in a country’s debt falls to ratings agencies like Fitch and Moody’s. But for the derivatives market, a committee of I.S.D.A. makes the call.

If the committee decides there was a default, it passes the baton to Markit, which is partly owned by the banks. Markit holds an auction to determine how much value has been lost on the debt, and that determines how much money is paid out to the parties that purchased the insurance.(...)

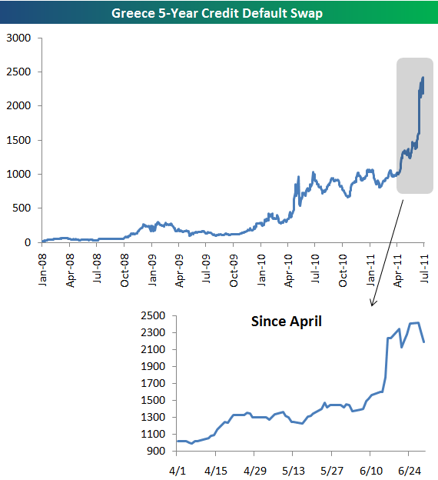

The uncertainty around how a sovereign default would course through the derivatives market had greatly increased the price premiums banks were charging to put on new derivatives trades related to European countries. As of last week, the price to insure against default on $10 million of Greek debt was $1.9 million per year, up from $775,000 a year ago, according to Markit.

“There is lack of transparency and visibility in these products, and that increases the risk,” said Marc Chandler, global head of currency strategy at Brown Brothers Harriman, a boutique banking firm in New York.

Ancora il 24 maggio il prezzo per assicurare 10 milioni di debito greco contro il default era di "solo" 1.4 milioni di dollari all'anno...

Ancora il 24 maggio il prezzo per assicurare 10 milioni di debito greco contro il default era di "solo" 1.4 milioni di dollari all'anno...Pochi giorni dopo la stesura dell'articolo sul NYTimes, che cita un prezzo di 1.9 milioni all'anno, ovvero circa 1900 punti base, il prezzo dei CDS sul debito greco è esploso raggiungendo il 24 giugno un massimo di 2421 punti base.

Anche se il parlamento greco ha votato per le misure di austerità i prezzi dei CDS sono comunque ancora molto ben oltre i 2200 punti base all'anno. I mercati sembrano ancora assolutamente scettici sulle speranze di evitare un default.

Se anche voi a volte vi ponete delle domande sul ruolo che i derivati, e specificatamente i CDS, svolgono nella redistribuzione del rischio tra i vari agenti potete dare un'occhiata a questo post e se vi incuriosite potete leggere questo working paper.

Nessun commento:

Posta un commento