Nessuno nutre dubbi sul fatto che la Cina si prepari al sorpasso degli USA...non sapevo però che questa era la norma nel XIX secolo, almeno fino al 1889! Potete leggere qui come l'OECD sia giunta a questa conclusione e divertirvi con lo script java qui sotto

Se invece volete andare oltre il GDP e siete interessati non solo allo sviluppo economico ma anche ad altri indicatori sociali e politici troverete interessante il Failed States Index 2009 che classifica i paesi sulla base dei 12 criteri che ho riportato qui sotto

Social Indicators

I-1. Mounting Demographic Pressures

I-2. Massive Movement of Refugees or Internally Displaced Persons creating

Complex Humanitarian Emergencies

I-3. Legacy of Vengeance-Seeking Group Grievance or Group Paranoia

I-4. Chronic and Sustained Human Flight

Economic Indicators

I-5. Uneven Economic Development along Group Lines

I-6. Sharp and/or Severe Economic Decline

Political Indicators

I-7. Criminalization and/or Delegitimization of the State

I-8. Progressive Deterioration of Public Services

I-9. Suspension or Arbitrary Application of the Rule of Law and Widespread

Violation of Human Rights

I-10. Security Apparatus Operates as a "State Within a State"

I-11. Rise of Factionalized Elites

I-12. Intervention of Other States or External Political Actors

Infine vi lascio con il link a un video in cui Nouriel Roubini e Jim O'Neill discutono della crisi del debito greco e delle prospettive della Cina, con due prospettive assolutamente divergenti.

mercoledì 31 marzo 2010

martedì 30 marzo 2010

Meglio le azioni delle obbligazioni? Fino a quando?

Secondo il leggendario Bill Gross di Pimco le azioni hanno ancora un po' di fiato e potrebbero riservare piacevoli sorprese, almeno fino all'estate

I mercati sono effficienti? Anche quelli emergenti? Secondo Burton Malkiel, intervistato dal Financial Times, assolutamente sì e raccomanda di investire passivamente in un indice azionario mondiale. Ecco gli ETF disponibili a Piazza Affari

I mercati sono effficienti? Anche quelli emergenti? Secondo Burton Malkiel, intervistato dal Financial Times, assolutamente sì e raccomanda di investire passivamente in un indice azionario mondiale. Ecco gli ETF disponibili a Piazza Affari

Se pensate che i mercati siano sì efficienti ma non del tutto potete anche prendere in considerazione etf che replicano indici fondamentali, in cui il peso di ogni società non è semplicemente determinato dalla capitalizzazione ma anche dai profitti, dai dividendi, ecc. Eccone un esempio

lunedì 29 marzo 2010

Until the end of the world: punks and plutocrats...

Fatta la riforma sanitaria sono le nuove regole per le banche e l'industria finanziaria USA a essere nel mirino della Casa Bianca. Dalle colonne del New York Times Paul Krugman non usa mezze misure per descrivere la polarizzazione delle posizioni tra punks and plutocrats:

Some background: we used to have a workable system for avoiding financial crises, resting on a combination of government guarantees and regulation. On one side, bank deposits were insured, preventing a recurrence of the immense bank runs that were a central cause of the Great Depression. On the other side, banks were tightly regulated, so that they didn’t take advantage of government guarantees by running excessive risks.

From 1980 or so onward, however, that system gradually broke down, partly because of bank deregulation, but mainly because of the rise of “shadow banking”: institutions and practices — like financing long-term investments with overnight borrowing — that recreated the risks of old-fashioned banking but weren’t covered either by guarantees or by regulation. The result, by 2007, was a financial system as vulnerable to severe crisis as the system of 1930. And the crisis came.

Now what? We have already, in effect, recreated New Deal-type guarantees: as the financial system plunged into crisis, the government stepped in to rescue troubled financial companies, so as to avoid a complete collapse. And you should bear in mind that the biggest bailouts took place under a conservative Republican administration, which claimed to believe deeply in free markets. There’s every reason to believe that this will be the rule from now on: when push comes to shove, no matter who is in power, the financial sector will be bailed out. In effect, debts of shadow banks, like deposits at conventional banks, now have a government guarantee.

The only question now is whether the financial industry will pay a price for this privilege, whether Wall Street will be obliged to behave responsibly in return for government backing. And who could be against that?

Well, how about John Boehner, the House minority leader? Recently Mr. Boehner gave a talk to bankers in which he encouraged them to balk efforts by Congress to impose stricter regulation. “Don’t let those little punk staffers take advantage of you, and stand up for yourselves,” he urged — where by “taking advantage” he meant imposing some conditions on the industry in return for government backing.

Barney Frank, the chairman of the House Financial Services Committee, promptly had “Little Punk Staffer” buttons made up and distributed to Congressional aides.(...)

The only question is whether we’re going to regulate bankers so that they don’t abuse the privilege of government backing. And it’s that regulation — not future bailouts — that reform opponents are trying to block.

So it’s the punks versus the plutocrats — those who want to rein in runaway banks, and bankers who want the freedom to put the economy at risk, freedom enhanced by the knowledge that taxpayers will bail them out in a crisis. Whatever they say, the fact is that people like Mr. Shelby are on the side of the plutocrats; the American people should be on the side of the punks, who are trying to protect their interests.

Sul ruolo che lo shadow banking system ha svolto nella crisi e sulla necessità di cambiare in profondità il suo modus operandi si occupa anche l'Economist anche se con accenti molto diversi da quelli di Krugman e dei liberals americani:

This “shadow” banking system is huge, particularly in America—too big for the banks to be able to replace it. In the summer of 2007 assets funded through the capital markets were larger than those held by America’s banks. Only one-third of the country’s home mortgages were on banks’ balance-sheets. The bank bail-outs hog attention, but many of the government’s crisis measures were designed to prop up the shadow system. Even so, many bits of it, especially private mortgage-backed securities, remain moribund (see article).

That is a bad thing. The intellectual case for securitisation, the process of pooling lots of different loans and selling the cashflows to investors, remains strong. Done properly, it should enable banks and investors to diversify their exposures. In Europe, where bank lending is more important, it offers a useful, alternative source of financing. But the shadow system has to become far more stable.(...)

So more attention is needed. But what should be done? Two things stand out. The first is the need to project some light into the shadows. (...) Investors need to have up-to-date information on the quality of the loans inside securities: central banks can help by mandating disclosure requirements for collateral that they accept at the discount window. And regulators need better data on obscure areas like triparty repo and stock lending.

The other imperative is to make sure that the bits of the shadow system that act just like banks are regulated accordingly. That shift in thinking has already happened for investment banks, but needs to go further. Money-market funds are an obvious example. Investors in these funds expect to get their money back on demand, just like depositors in a bank. The post-Lehman run started after one fund “broke the buck”; it stopped when the government said it would guarantee investors against losses. So these funds should be forced to make a choice: keep the commitment to pay up and set aside capital and insurance funds (like banks have to do); or drop the commitment and put the burden of losses on investors.

Lasciando da parte il dibattito sulla regolamentazione vi segnalo brevemente alcuni articoli:

Some background: we used to have a workable system for avoiding financial crises, resting on a combination of government guarantees and regulation. On one side, bank deposits were insured, preventing a recurrence of the immense bank runs that were a central cause of the Great Depression. On the other side, banks were tightly regulated, so that they didn’t take advantage of government guarantees by running excessive risks.

From 1980 or so onward, however, that system gradually broke down, partly because of bank deregulation, but mainly because of the rise of “shadow banking”: institutions and practices — like financing long-term investments with overnight borrowing — that recreated the risks of old-fashioned banking but weren’t covered either by guarantees or by regulation. The result, by 2007, was a financial system as vulnerable to severe crisis as the system of 1930. And the crisis came.

Now what? We have already, in effect, recreated New Deal-type guarantees: as the financial system plunged into crisis, the government stepped in to rescue troubled financial companies, so as to avoid a complete collapse. And you should bear in mind that the biggest bailouts took place under a conservative Republican administration, which claimed to believe deeply in free markets. There’s every reason to believe that this will be the rule from now on: when push comes to shove, no matter who is in power, the financial sector will be bailed out. In effect, debts of shadow banks, like deposits at conventional banks, now have a government guarantee.

The only question now is whether the financial industry will pay a price for this privilege, whether Wall Street will be obliged to behave responsibly in return for government backing. And who could be against that?

Well, how about John Boehner, the House minority leader? Recently Mr. Boehner gave a talk to bankers in which he encouraged them to balk efforts by Congress to impose stricter regulation. “Don’t let those little punk staffers take advantage of you, and stand up for yourselves,” he urged — where by “taking advantage” he meant imposing some conditions on the industry in return for government backing.

Barney Frank, the chairman of the House Financial Services Committee, promptly had “Little Punk Staffer” buttons made up and distributed to Congressional aides.(...)

The only question is whether we’re going to regulate bankers so that they don’t abuse the privilege of government backing. And it’s that regulation — not future bailouts — that reform opponents are trying to block.

So it’s the punks versus the plutocrats — those who want to rein in runaway banks, and bankers who want the freedom to put the economy at risk, freedom enhanced by the knowledge that taxpayers will bail them out in a crisis. Whatever they say, the fact is that people like Mr. Shelby are on the side of the plutocrats; the American people should be on the side of the punks, who are trying to protect their interests.

Sul ruolo che lo shadow banking system ha svolto nella crisi e sulla necessità di cambiare in profondità il suo modus operandi si occupa anche l'Economist anche se con accenti molto diversi da quelli di Krugman e dei liberals americani:

This “shadow” banking system is huge, particularly in America—too big for the banks to be able to replace it. In the summer of 2007 assets funded through the capital markets were larger than those held by America’s banks. Only one-third of the country’s home mortgages were on banks’ balance-sheets. The bank bail-outs hog attention, but many of the government’s crisis measures were designed to prop up the shadow system. Even so, many bits of it, especially private mortgage-backed securities, remain moribund (see article).

That is a bad thing. The intellectual case for securitisation, the process of pooling lots of different loans and selling the cashflows to investors, remains strong. Done properly, it should enable banks and investors to diversify their exposures. In Europe, where bank lending is more important, it offers a useful, alternative source of financing. But the shadow system has to become far more stable.(...)

Towards a penumbral banking system

So far the reformers of finance have neglected the shadow system. Some changes are on the way—new liquidity rules for money-market funds, for instance.(...)So more attention is needed. But what should be done? Two things stand out. The first is the need to project some light into the shadows. (...) Investors need to have up-to-date information on the quality of the loans inside securities: central banks can help by mandating disclosure requirements for collateral that they accept at the discount window. And regulators need better data on obscure areas like triparty repo and stock lending.

The other imperative is to make sure that the bits of the shadow system that act just like banks are regulated accordingly. That shift in thinking has already happened for investment banks, but needs to go further. Money-market funds are an obvious example. Investors in these funds expect to get their money back on demand, just like depositors in a bank. The post-Lehman run started after one fund “broke the buck”; it stopped when the government said it would guarantee investors against losses. So these funds should be forced to make a choice: keep the commitment to pay up and set aside capital and insurance funds (like banks have to do); or drop the commitment and put the burden of losses on investors.

Lasciando da parte il dibattito sulla regolamentazione vi segnalo brevemente alcuni articoli:

- da più parti ci si interroga sempre più perplessi sulle ragioni del prplungarsi del rally azionario: qui trovate un ventaglio di opinioni raccolte dal New York Times;

- Lavoce propone un articolo di Yiping Huang contrario alle rappresaglie USA contro la sottovalutazione della valuta cinese; per altre notizie su come il cambio sia visto da Pechino potete leggere qui;

- la capitalizzazione delle borse mondiali si aggira intorno ai 47000 miliardi di dollari USA, la borsa di Milano si ferma ad appena 650 miliardi. Date un'occhiata qui al confronto tra le diverse borse e scoprirete che la borsa di Seoul vale il 30% in più di Milano.

domenica 28 marzo 2010

Day trading? La ricchezza delle regioni italiane. Prevedere i rendimenti futuri dell'indice S&P500

Questo post di TraderMark su SeekingAlpha mi ha fatto sorridere e ve lo segnalo.

Volete dedicarvi al day trading? A me non pare una buona idea, comunque troverete forse interessante questo articolo del New York Times

Oggi e domani ci sono le elezioni regionali: trovate qui e qui e tabelle comparative

Volete dedicarvi al day trading? A me non pare una buona idea, comunque troverete forse interessante questo articolo del New York Times

Oggi e domani ci sono le elezioni regionali: trovate qui e qui e tabelle comparative

dei principali indicatori economici delle regioni in cui è in corso la votazione, raccolte da www.lavoce.info. Secondo gli autori (Fonte: Istat, Eurostat - elaborazione dati Davide Baldi e Ludovico Poggi) raffrontando le regioni tra loro e rispetto alle medie nazionali, i lettori possono farsi un'idea dello sviluppo economico e civile raggiunto nei diversi territori, nonché della qualità dei loro governi.

Infine vi segnalo un interessante post di Prieur du Plessis su Seekingalpha:

Infine vi segnalo un interessante post di Prieur du Plessis su Seekingalpha:

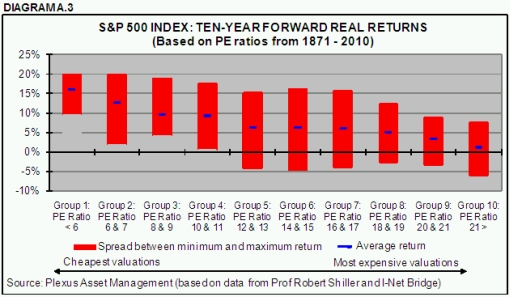

il tentativo è di prevedere i rendimenti azionari su una scala di tempo lunga (10 anni) utilizzando la metodologia di Robert Shiller che impiega come predittore il rapporto prezzo/utili dell'indice S&P500 mediato sugli ultimi 10 anni di profitti reali (deflazionati) aggregati dell'indice. L'evidenza a supporto di questa relazione è robusta come mostra la prima delle figure qui accanto. Invece del rapporto prezzo su utili si possono utilizzare i dividendi (anch'essi deflazionati e mediati su dieci anni) giungendo a conclusioni molto simili.

il tentativo è di prevedere i rendimenti azionari su una scala di tempo lunga (10 anni) utilizzando la metodologia di Robert Shiller che impiega come predittore il rapporto prezzo/utili dell'indice S&P500 mediato sugli ultimi 10 anni di profitti reali (deflazionati) aggregati dell'indice. L'evidenza a supporto di questa relazione è robusta come mostra la prima delle figure qui accanto. Invece del rapporto prezzo su utili si possono utilizzare i dividendi (anch'essi deflazionati e mediati su dieci anni) giungendo a conclusioni molto simili.

Le conclusioni non sono troppo incorraggianti:

I dati necessari per riprodurre le analisi riportate sopra sono messi a disposizione da Robert Shiller sulla sua pagina web. Conoscete qualche link dove poter trovare gli stessi dati (magari solo per 30-40 anni anziche per 140 anni) per altri indici azionari? Per esempio per azioni inglesi o giapponesi?

il tentativo è di prevedere i rendimenti azionari su una scala di tempo lunga (10 anni) utilizzando la metodologia di Robert Shiller che impiega come predittore il rapporto prezzo/utili dell'indice S&P500 mediato sugli ultimi 10 anni di profitti reali (deflazionati) aggregati dell'indice. L'evidenza a supporto di questa relazione è robusta come mostra la prima delle figure qui accanto. Invece del rapporto prezzo su utili si possono utilizzare i dividendi (anch'essi deflazionati e mediati su dieci anni) giungendo a conclusioni molto simili.

il tentativo è di prevedere i rendimenti azionari su una scala di tempo lunga (10 anni) utilizzando la metodologia di Robert Shiller che impiega come predittore il rapporto prezzo/utili dell'indice S&P500 mediato sugli ultimi 10 anni di profitti reali (deflazionati) aggregati dell'indice. L'evidenza a supporto di questa relazione è robusta come mostra la prima delle figure qui accanto. Invece del rapporto prezzo su utili si possono utilizzare i dividendi (anch'essi deflazionati e mediati su dieci anni) giungendo a conclusioni molto simili.Le conclusioni non sono troppo incorraggianti:

Based on the above research findings, with the S&P 500 Index’s current ten-year normalized PE of 20.3 and ten-year normalized dividend yield of 2.1%, investors should be aware of the fact that the market is by historical standards expensive. As far as the market in general is concerned, this argues for unexciting long-term returns, possibly a “muddle-through” trading range for quite a number of years to come.

Although the research results offer no guidance as to calling market tops and bottoms, they do indicate that it would not be consistent with the findings to bank on above-average returns based on the current ten-year normalized valuation levels. As a matter of fact, there is a distinct possibility of some negative returns off current price levels.

I dati necessari per riprodurre le analisi riportate sopra sono messi a disposizione da Robert Shiller sulla sua pagina web. Conoscete qualche link dove poter trovare gli stessi dati (magari solo per 30-40 anni anziche per 140 anni) per altri indici azionari? Per esempio per azioni inglesi o giapponesi?

sabato 27 marzo 2010

Una lunga marcia per Atene. Innovazione di stato: si o no? Aggiornamento al 26 marzo 2010.

Negli ultimi due giorni l'euro ha ripreso un po' di fato sul dollaro dopo un inizio di settimana disastroso e dopo che si e' raggiunto un accordo per sostenere la Grecia con una linea di credito di circa 22 miliardi di euro finanziata da prestiti bilaterali e dall'FMI. Secondo il New York Times:

After months of fractious debate, the 16 countries that use the euro agreed on a financial safety net for Greece, combining bilateral loans from those European nations with cash from the International Monetary Fund.

The deal emerged as the European Central Bank said on Thursday that it would hold off tightening lending rules until 2011, a move that appeared to be intended to help Greek banks in particular. Mr. Trichet told the European Parliament that the central bank would keep the credit ratings at an exceptionally low level for longer than planned on the collateral that its accepts from banks in return for short-term loans.

Previously, the central bank had said that it would raise the threshold for collateral at the end of 2010. It had been lowered as an extraordinary measure to help banks in the euro zone weather the global credit crisis.(...)

The bank’s decision should have “positive implications” not only for Greece, they said, but also for other countries under pressure along Europe’s periphery, like Portugal, which was downgraded on Wednesday by Fitch Ratings.

More details of the changes will be announced at the central bank’s next council meeting on April 8. Greece’s long-term foreign currency rating is A2 from Moody’s and BBB+ from Standard & Poor’s. For its operations, the European Central Bank had until now said that the current minimum credit threshold of BBB- would revert to A- at the end of 2010.

Now, for Greek government bonds to be excluded from European Central Bank operations, they would have to be downgraded five times by Moody’s and three times by Fitch and S.& P., analysts said.

“No doubt the worries about Greek government bonds remaining eligible at the E.C.B. beyond the end of 2010 have played a role in accelerating the decision to modify the framework, which in itself is not surprising,” Laurent Fransolet, an analyst at Barclays Capital in London, wrote in a note to clients.

Secondo l'Economist si tratta pero' di una goccia destinata a perdersi nel mare del debito greco, utile soprattutto a guadagnare tempo:

(...) That may be enough to calm markets and enable Greece to roll over its debts. But it will be only a temporary fix. It will take years to repair Greece’s public finances, which means a much larger rescue fund will be needed if it is to avoid default. The Greek government has somehow to keep its economy on an even keel while pushing through a huge fiscal tightening. Countries that seek IMF help generally have to endure brutal cuts in public spending, which deepen recessions. To counter that effect, the IMF typically counsels a weaker currency. Sadly, this is not an option for Greece. Stuck in the euro, its exchange rate with its main trading partners is fixed. Greece cannot devalue, so it needs more time to adjust than the three years it has agreed with its EU partners—and a bigger safety net while it does.

The Greek government has somehow to keep its economy on an even keel while pushing through a huge fiscal tightening. Countries that seek IMF help generally have to endure brutal cuts in public spending, which deepen recessions. To counter that effect, the IMF typically counsels a weaker currency. Sadly, this is not an option for Greece. Stuck in the euro, its exchange rate with its main trading partners is fixed. Greece cannot devalue, so it needs more time to adjust than the three years it has agreed with its EU partners—and a bigger safety net while it does.

Just how big? Analysis by The Economist suggests a figure of €75 billion rather than €25 billion. Greece is likely to need five years to get its deficit down below 3% of GDP (see table). On our projections interest payments will rise from 5% of GDP to 8.4% in that time, to reflect the higher cost of issuing new debts and of refinancing old ones. Other budgetary cuts will be needed to offset this. By our reckoning the Greek government will have to increase the “primary” budget balance (ie, excluding interest payments) by 13.5 percentage points of GDP to cap its debt burden. That is bound to have an effect on growth. Our projections assume that nominal GDP will be 5% lower by 2014.

Qui trovate una tabellina con le proiezioni dal 2009 al 2014.

Sempre su l'Economist trovate un aggiornamento sulla crisi del Dubai. Inoltre fino a domenica potete partecipare al

dibattito dell'Economist sul ruolo dei governi nel promuovere l'innovazione: al momento l'esito e' assolutamente incerto ed equilibrato.

Ecco l'aggiornamento al 26 marzo.

After months of fractious debate, the 16 countries that use the euro agreed on a financial safety net for Greece, combining bilateral loans from those European nations with cash from the International Monetary Fund.

The proposal, brokered by France and Germany and then approved by European leaders on Thursday, would take effect if the Greek government were unable to borrow in the commercial markets. Under the deal, loans would be provided at market rates and offered only with the agreement of all the nations that use the euro currency.(...)

The agreement said the euro zone countries would be expected to contribute based on the amount each makes available to the European Central Bank’s capital reserves.(...)The deal emerged as the European Central Bank said on Thursday that it would hold off tightening lending rules until 2011, a move that appeared to be intended to help Greek banks in particular. Mr. Trichet told the European Parliament that the central bank would keep the credit ratings at an exceptionally low level for longer than planned on the collateral that its accepts from banks in return for short-term loans.

Previously, the central bank had said that it would raise the threshold for collateral at the end of 2010. It had been lowered as an extraordinary measure to help banks in the euro zone weather the global credit crisis.(...)

The bank’s decision should have “positive implications” not only for Greece, they said, but also for other countries under pressure along Europe’s periphery, like Portugal, which was downgraded on Wednesday by Fitch Ratings.

More details of the changes will be announced at the central bank’s next council meeting on April 8. Greece’s long-term foreign currency rating is A2 from Moody’s and BBB+ from Standard & Poor’s. For its operations, the European Central Bank had until now said that the current minimum credit threshold of BBB- would revert to A- at the end of 2010.

Now, for Greek government bonds to be excluded from European Central Bank operations, they would have to be downgraded five times by Moody’s and three times by Fitch and S.& P., analysts said.

“No doubt the worries about Greek government bonds remaining eligible at the E.C.B. beyond the end of 2010 have played a role in accelerating the decision to modify the framework, which in itself is not surprising,” Laurent Fransolet, an analyst at Barclays Capital in London, wrote in a note to clients.

Secondo l'Economist si tratta pero' di una goccia destinata a perdersi nel mare del debito greco, utile soprattutto a guadagnare tempo:

(...) That may be enough to calm markets and enable Greece to roll over its debts. But it will be only a temporary fix. It will take years to repair Greece’s public finances, which means a much larger rescue fund will be needed if it is to avoid default.

The Greek government has somehow to keep its economy on an even keel while pushing through a huge fiscal tightening. Countries that seek IMF help generally have to endure brutal cuts in public spending, which deepen recessions. To counter that effect, the IMF typically counsels a weaker currency. Sadly, this is not an option for Greece. Stuck in the euro, its exchange rate with its main trading partners is fixed. Greece cannot devalue, so it needs more time to adjust than the three years it has agreed with its EU partners—and a bigger safety net while it does.

The Greek government has somehow to keep its economy on an even keel while pushing through a huge fiscal tightening. Countries that seek IMF help generally have to endure brutal cuts in public spending, which deepen recessions. To counter that effect, the IMF typically counsels a weaker currency. Sadly, this is not an option for Greece. Stuck in the euro, its exchange rate with its main trading partners is fixed. Greece cannot devalue, so it needs more time to adjust than the three years it has agreed with its EU partners—and a bigger safety net while it does. Just how big? Analysis by The Economist suggests a figure of €75 billion rather than €25 billion. Greece is likely to need five years to get its deficit down below 3% of GDP (see table). On our projections interest payments will rise from 5% of GDP to 8.4% in that time, to reflect the higher cost of issuing new debts and of refinancing old ones. Other budgetary cuts will be needed to offset this. By our reckoning the Greek government will have to increase the “primary” budget balance (ie, excluding interest payments) by 13.5 percentage points of GDP to cap its debt burden. That is bound to have an effect on growth. Our projections assume that nominal GDP will be 5% lower by 2014.

Qui trovate una tabellina con le proiezioni dal 2009 al 2014.

Sempre su l'Economist trovate un aggiornamento sulla crisi del Dubai. Inoltre fino a domenica potete partecipare al

dibattito dell'Economist sul ruolo dei governi nel promuovere l'innovazione: al momento l'esito e' assolutamente incerto ed equilibrato.

Ecco l'aggiornamento al 26 marzo.

venerdì 26 marzo 2010

Se le banche fossero semplici e simili alle utilities?

Ho trovato molto interessante l'analisi della nuova avventura di Sir Richard Branson svolta da Steve Worthington, e Peter Welch e distribuita qualche giorno fa nella newsletter settimanale del Capco institute.

Lo riproduco qui con l'autorizzazione di uno degli autori (grazie Peter!)

Industry watchers should keep a close eye on the U.K., which is set to become a fascinating test case on the future of banking. In the wake of the crisis, both Sir Richard Branson’s multi-sector Virgin Group and retailing giant Tesco have announced plans to offer full-service retail banking. And both are ambitious to do banking differently. Virgin Money wants “to offer a new kind of bank in the U.K. - one where everyone benefits.” Tesco Bank says it will focus on “being simple, straightforward and rewarding loyalty.”

How likely are they to make an impact? Can they really bring a new approach to retail banking? We have recently completed a research study assessing the prospects for Virgin Money and Tesco Bank. For all the excitement around their plans, our research indicates it will not be easy.

Of course, the suggestion that ‘non-banks’ such as retailers might shake-up retail banking long pre-dates the crisis. A 1994 study for the American Bankers' Roundtable concluded that "banking is essential to a modern economy; banks are not." Indeed, both Virgin and Tesco first ventured into financial services as long ago as the mid-1990s. However, until the crisis, both were niche players, concentrating on a select range of products and operating through partnerships with existing banks. Tesco operated through a joint venture with RBS, only buying out its banking partner at the end of 2008. Virgin Money also partnered with RBS along with other financial services companies. It launched but then sold its stake in the innovative “One Account” mortgage joint venture with RBS, though for the moment it remains an introducer for the business.

Does the impact of the crisis justify a step up from niche players to full-service retail banks? Clearly, the post-crisis unpopularity of existing banks makes new entrants potentially more attractive. But set against this, banking is becoming less profitable, making the market less attractive. And despite the crisis, the established banks’ branch networks, infrastructure, and customer relationships remain remarkably well-entrenched.

In reality, for all the excitement, there are major hurdles that ‘non-banks’ like Virgin and Tesco face in building full-service banks:

• Despite all the moves by regulators to facilitate account switching, U.K. consumers remain instinctively relucant to change their current (checking) account.

• Further, U.K. banks are reliant on opaque means of generating revenue from their current accounts, namely high overdraft charges and little or no interest paid on credit balances. This is in return for notionally free banking. The recent failure of the U.K.‘s Office of Fair Trading legal challenge to unauthorised overdraft charges reduces the pressure for new pricing models and may hence be a further impediment to ‘new’ entrants.

• If Virgin and Tesco rely on these same pricing models, will they lose their reputational advantage? But if they charge customers a fee for current accounts, will U.K. consumers be willing to drop their deep attachment to ‘free-in-credit’ banking?

• With much reduced access to wholesale funding following the crisis, Virgin and Tesco will need to build large deposit bases in order to offer services such as mortgages. But they face intense competition for retail deposits from existing banks and building societies (mutual thrifts).

• Like many banks, Virgin Money and Tesco Bank relied heavily on credit cards and consumer credit before the crisis to drive their own financial services businesses. However, in the wake of the crisis, prospects for credit cards are bleak. And no other banking segment offers an equivalent ’growth engine’ to support their push into full-service banking.

Further, despite both offering financial services for more than a decade, the current operations of Virgin Money and Tesco Bank are small relative to the established banks. The only way for Virgin or Tesco to achieve scale quickly would be through a major acquisition. The U.K. government’s planned sale of mortgage lender Northern Rock and divestments imposed on Lloyds and RBS by the European Commission may present opportunities. Virgin originally expressed an interest in acquiring Northern Rock back in the early days of the crisis. But acquisitions on this scale (Northern Rock’s retail savings balances are approximately four times those of Tesco Bank) would carry significant integration risks and require a significant capital investment.

From the perspective of competition and consumer choice, the banking ambitions of Virgin and Tesco are clearly welcome. And for all those that follow developments in banking, it will be fascinating to watch. This is an attempt to do banking without the banks on a scale not seen before. Virgin has already signalled it is prepared to challenge the ‘free-in-credit’ model that dominates personal banking in the UK. But even brands as strong as Tesco and Virgin may find it tough to shake-up as conservative a market as retail banking.

Lo riproduco qui con l'autorizzazione di uno degli autori (grazie Peter!)

Virgin and Tesco shouldn’t bank on an easy ride

Steve Worthington, Professor of Marketing, Monash University, and Peter Welch, Founder, BankEcon.com

Clearly, the financial crisis is leading to major changes in the capital, liquidity, and accounting regimes for banks. But might the crisis also open up the sector to non-bank competitors on a scale not seen before? Is the distrust of mainstream banks now so deep that ambitious companies in other sectors have an unparalleled opportunity to become major providers of banking services?Industry watchers should keep a close eye on the U.K., which is set to become a fascinating test case on the future of banking. In the wake of the crisis, both Sir Richard Branson’s multi-sector Virgin Group and retailing giant Tesco have announced plans to offer full-service retail banking. And both are ambitious to do banking differently. Virgin Money wants “to offer a new kind of bank in the U.K. - one where everyone benefits.” Tesco Bank says it will focus on “being simple, straightforward and rewarding loyalty.”

How likely are they to make an impact? Can they really bring a new approach to retail banking? We have recently completed a research study assessing the prospects for Virgin Money and Tesco Bank. For all the excitement around their plans, our research indicates it will not be easy.

Of course, the suggestion that ‘non-banks’ such as retailers might shake-up retail banking long pre-dates the crisis. A 1994 study for the American Bankers' Roundtable concluded that "banking is essential to a modern economy; banks are not." Indeed, both Virgin and Tesco first ventured into financial services as long ago as the mid-1990s. However, until the crisis, both were niche players, concentrating on a select range of products and operating through partnerships with existing banks. Tesco operated through a joint venture with RBS, only buying out its banking partner at the end of 2008. Virgin Money also partnered with RBS along with other financial services companies. It launched but then sold its stake in the innovative “One Account” mortgage joint venture with RBS, though for the moment it remains an introducer for the business.

Does the impact of the crisis justify a step up from niche players to full-service retail banks? Clearly, the post-crisis unpopularity of existing banks makes new entrants potentially more attractive. But set against this, banking is becoming less profitable, making the market less attractive. And despite the crisis, the established banks’ branch networks, infrastructure, and customer relationships remain remarkably well-entrenched.

In reality, for all the excitement, there are major hurdles that ‘non-banks’ like Virgin and Tesco face in building full-service banks:

• Despite all the moves by regulators to facilitate account switching, U.K. consumers remain instinctively relucant to change their current (checking) account.

• Further, U.K. banks are reliant on opaque means of generating revenue from their current accounts, namely high overdraft charges and little or no interest paid on credit balances. This is in return for notionally free banking. The recent failure of the U.K.‘s Office of Fair Trading legal challenge to unauthorised overdraft charges reduces the pressure for new pricing models and may hence be a further impediment to ‘new’ entrants.

• If Virgin and Tesco rely on these same pricing models, will they lose their reputational advantage? But if they charge customers a fee for current accounts, will U.K. consumers be willing to drop their deep attachment to ‘free-in-credit’ banking?

• With much reduced access to wholesale funding following the crisis, Virgin and Tesco will need to build large deposit bases in order to offer services such as mortgages. But they face intense competition for retail deposits from existing banks and building societies (mutual thrifts).

• Like many banks, Virgin Money and Tesco Bank relied heavily on credit cards and consumer credit before the crisis to drive their own financial services businesses. However, in the wake of the crisis, prospects for credit cards are bleak. And no other banking segment offers an equivalent ’growth engine’ to support their push into full-service banking.

Further, despite both offering financial services for more than a decade, the current operations of Virgin Money and Tesco Bank are small relative to the established banks. The only way for Virgin or Tesco to achieve scale quickly would be through a major acquisition. The U.K. government’s planned sale of mortgage lender Northern Rock and divestments imposed on Lloyds and RBS by the European Commission may present opportunities. Virgin originally expressed an interest in acquiring Northern Rock back in the early days of the crisis. But acquisitions on this scale (Northern Rock’s retail savings balances are approximately four times those of Tesco Bank) would carry significant integration risks and require a significant capital investment.

From the perspective of competition and consumer choice, the banking ambitions of Virgin and Tesco are clearly welcome. And for all those that follow developments in banking, it will be fascinating to watch. This is an attempt to do banking without the banks on a scale not seen before. Virgin has already signalled it is prepared to challenge the ‘free-in-credit’ model that dominates personal banking in the UK. But even brands as strong as Tesco and Virgin may find it tough to shake-up as conservative a market as retail banking.

mercoledì 24 marzo 2010

Fondi hedge per tutti?

Hedge funds per le masse? A sentire Marketwatch si direbbe di sì:

The number of mutual funds attempting to replicate hedge fund strategies has risen dramatically, with 80% of today's long-short funds launched in just the past few years. The funds have come from both mutual fund firms branching into a new area and hedge fund managers making their strategies available in mutual fund formats.

But is this type of fund right for you? A hedge fund-style strategy should in theory deliver returns independent of the stock market -- a fact that appeals to many investors still smarting from the market's meltdown in 2008 and early 2009.

Indeed, hedge funds seem to have weathered that storm much better than mutual funds. Data from Hedge Fund Research Inc. show that the HFRI Fund Weighted Composite Index fell 19% in 2008, versus a loss of more than 40% for the average stock mutual fund.

Se vi interessa avvicinarvi al mondo degli hedge funds ma siete impreparati potete iniziare leggendo la voce hedge fund su Wikipedia. Richard Wilson ha un blog interamente dedicato all'industria degli hedge funds.

Gli indici più famosi di hedge funds sono mantenuti da HFRX e li trovate qui. Infine se volete provare a clonare le strategie degli hedge funds più popolari potete provare a seguire quanto suggerito da alphaclone.

The number of mutual funds attempting to replicate hedge fund strategies has risen dramatically, with 80% of today's long-short funds launched in just the past few years. The funds have come from both mutual fund firms branching into a new area and hedge fund managers making their strategies available in mutual fund formats.

Investors have responded: in 2009 long-short mutual funds and saw more than $10 billion in net inflows, double their previous annual high, in 2006, according to investment researcher Morningstar Inc.

A move of hedge fund-style strategies into mutual funds could be a win for all concerned: investors could see steadier returns while traditional hedge fund firms open their doors to more clients. For mutual fund firms, these funds can be a way to attract new money in choppy markets and also keep investors from fleeing during times of panic. But is this type of fund right for you? A hedge fund-style strategy should in theory deliver returns independent of the stock market -- a fact that appeals to many investors still smarting from the market's meltdown in 2008 and early 2009.

Indeed, hedge funds seem to have weathered that storm much better than mutual funds. Data from Hedge Fund Research Inc. show that the HFRI Fund Weighted Composite Index fell 19% in 2008, versus a loss of more than 40% for the average stock mutual fund.

Se vi interessa avvicinarvi al mondo degli hedge funds ma siete impreparati potete iniziare leggendo la voce hedge fund su Wikipedia. Richard Wilson ha un blog interamente dedicato all'industria degli hedge funds.

Gli indici più famosi di hedge funds sono mantenuti da HFRX e li trovate qui. Infine se volete provare a clonare le strategie degli hedge funds più popolari potete provare a seguire quanto suggerito da alphaclone.

martedì 23 marzo 2010

Iperinflazione, stagflazione o deflazione?

In molti si interrogano sul rischio che l'imponente accumulo di debito sovrano sia l'anticamera di un periodo di iperinflazione.

L'opinione di Paul Krugman sulla questione (iper)inflazione/stagflazione è netta:

Hyperinflation is actually a quite well understood phenomenon, and its causes aren’t especially controversial among economists. It’s basically about revenue: when governments can’t either raise taxes or borrow to pay for their spending, they sometimes turn to the printing press, trying to extract large amounts of seignorage — revenue from money creation. This leads to inflation, which leads people to hold down their cash holdings, which means that the printing presses have to run faster to buy the same amount of resources, and so on.

The kind of inflation we had in the 1970s, the famous era of stagflation — high inflation combined with high unemployment — was quite different. Deficits weren’t the issue — actually, US deficits were much smaller in the inflationary 70s than in the disinflationary 80s. Instead, what you had was a combination of excessively expansionary monetary policies, based on an unrealistic view of how low the unemployment rate could be pushed without causing accelerating inflation (the NAIRU), plus oil shocks that pushed up inflation across the board thanks to widespread cost-of-living clauses in contracts. There was never any risk of hyperinflation; the only question was whether and when we’d be willing to pay the price in high unemployment of bringing inflation back down.(...)

Meanwhile, for those predicting hyperinflation, my question would be: what is it about the United States now that looks different to you from Japan in say, 2000? Big budget deficits and high debt? Check. Huge expansion in the monetary base? Check. And yet Japan’s GDP deflator has fallen 9 percent since 2000.

Gli fa eco Brad De Long su SeekingAlpha che aggiunge altre ragioni per non temere l'inflazione negli USA:

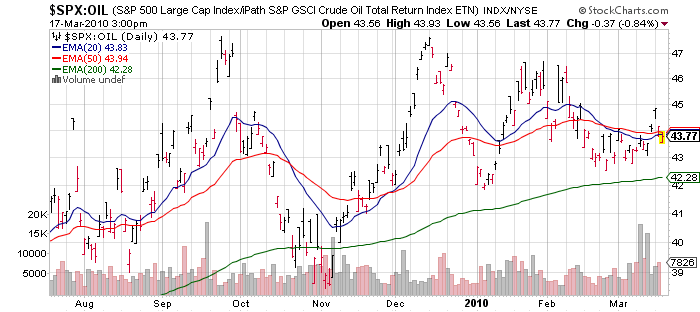

Comunque, se siete scettici e continuate a fare brutti sogni sull'inflazione, potete tenere d'occhio le materie prime e l'oro. Un modo divertente è seguire l'indice Dow Jones valutato in oro o in petrolio come in questo post dal quale ho preso i grafici che riproduco qui sotto

Ed ecco un grafico del rapporto Dow Jones / oro dal 1978 ad oggi

L'opinione di Paul Krugman sulla questione (iper)inflazione/stagflazione è netta:

Hyperinflation is actually a quite well understood phenomenon, and its causes aren’t especially controversial among economists. It’s basically about revenue: when governments can’t either raise taxes or borrow to pay for their spending, they sometimes turn to the printing press, trying to extract large amounts of seignorage — revenue from money creation. This leads to inflation, which leads people to hold down their cash holdings, which means that the printing presses have to run faster to buy the same amount of resources, and so on.

The kind of inflation we had in the 1970s, the famous era of stagflation — high inflation combined with high unemployment — was quite different. Deficits weren’t the issue — actually, US deficits were much smaller in the inflationary 70s than in the disinflationary 80s. Instead, what you had was a combination of excessively expansionary monetary policies, based on an unrealistic view of how low the unemployment rate could be pushed without causing accelerating inflation (the NAIRU), plus oil shocks that pushed up inflation across the board thanks to widespread cost-of-living clauses in contracts. There was never any risk of hyperinflation; the only question was whether and when we’d be willing to pay the price in high unemployment of bringing inflation back down.(...)

Meanwhile, for those predicting hyperinflation, my question would be: what is it about the United States now that looks different to you from Japan in say, 2000? Big budget deficits and high debt? Check. Huge expansion in the monetary base? Check. And yet Japan’s GDP deflator has fallen 9 percent since 2000.

Gli fa eco Brad De Long su SeekingAlpha che aggiunge altre ragioni per non temere l'inflazione negli USA:

I would add:

- The people putting their money on the line in financial markets are really, really, really not expecting any inflation.

- The inflation bugs have been expecting an imminent rise in inflation within the year for two and a half years now--since the fall of 2007; thus there is something wrong with their analysis.

- If there were signs of inflation we would be in a much healthier situation--because people would then be trying to buy real assets rather than Treasury bonds with their money, and that would push demand up and unemployment down.

Comunque, se siete scettici e continuate a fare brutti sogni sull'inflazione, potete tenere d'occhio le materie prime e l'oro. Un modo divertente è seguire l'indice Dow Jones valutato in oro o in petrolio come in questo post dal quale ho preso i grafici che riproduco qui sotto

Ed ecco un grafico del rapporto Dow Jones / oro dal 1978 ad oggi

lunedì 22 marzo 2010

Ancora sulla Grecia. L'ecologia dell'intelligenza negli USA. Come evitare di dover salvare le banche un'altra volta?

Vi raccomando il breve documentario sulla crisi del debito greco realizzato dal Wall Street Journal: potete guardarlo qui sotto:

Qui invece trovate gli articoli che il WSJ sta dedicando alla crisi greca.

Eccellente articolo di Thomas Friedman sul New York Times: riassume bene una delle ragioni per cui ammiro gli USA e per cui continuo ad essere un acceso sostenitore dell'ecologia dei cervelli (la necessità di costruire un habitat sociale ed economico che coltivi le idee innovative e le persone creative, indipendentemente da ogni altra loro caratteristica) mentre non sopporto la retorica del ritorno dei cervelli (se li fai tornare per farli rimbecillire a che serve farli rientrare?). Certo che gli USA devono curare alcuni dei loro (e non solo loro) mali se desiderano restare il paese di riferimento per libertà di iniziativa e innovazione: l'Op-Ed di Frank Rich sul Times di oggi sviluppa alcuni spunti di riflessione.

Intanto che l'America riflette su come migliorarsi,

l'Economist dedica un'analisi alla crescita della produttività negli USA, al cui confronto l'Europa impallidisce. Vorrei attirare la vostra attenzione sul confronto tra il tasso di crescita annuale della produttività negli USA e in Italia nel decennio 1998-2008: 2.2% vs. 0.4%. In un decennio questo porta ad una differenza del 20% A me sembra un dato significativo. Anche le previsioni per i prossimi 10 anni, nei quali la produttività USA dovrebbe crescere solo dell'1.5%, contro lo 0.5% italico, sono disarmanti.

l'Economist dedica un'analisi alla crescita della produttività negli USA, al cui confronto l'Europa impallidisce. Vorrei attirare la vostra attenzione sul confronto tra il tasso di crescita annuale della produttività negli USA e in Italia nel decennio 1998-2008: 2.2% vs. 0.4%. In un decennio questo porta ad una differenza del 20% A me sembra un dato significativo. Anche le previsioni per i prossimi 10 anni, nei quali la produttività USA dovrebbe crescere solo dell'1.5%, contro lo 0.5% italico, sono disarmanti.

Dopo due decenni così basteranno tre lavoratori USA per produrre lo stesso output orario di quattro lavoratori italiani.

Sul tema della riforma delle banche e della regolamentazione il punto di vista della Fed e della amministrazione Obama sembrano avvicinarsi

mentre sembra chiara l'intenzione del comitato di Basilea di evitare un ripetersi dei bailouts del 2008:

the final report of the Cross-Border Bank Resolution Group of the Basel Committee called for “firm-specific contingency planning” that would help the most interconnected financial companies survive a crisis or, if necessary, be dismantled in an orderly fashion, without risking a global financial crisis.

Il rapporto completo è disponibile a questo link ed ecco il comunicato stampa che lo annuncia:

The Basel Committee on Banking Supervision today issued its final Report and Recommendations of the Cross-border Bank Resolution Group.

Mr Nout Wellink, Chairman of the Basel Committee and President of the Netherlands Bank, noted that "the resolution of a cross-border bank is a complex and multidimensional process and the financial crisis exposed gaps in intervention techniques and tools needed for an orderly resolution. Based on the lessons of the crisis and our analysis of national resolution frameworks, I believe that implementation of the Committee's recommendations will help make meaningful progress toward addressing systemic risk and the too-big-to-fail problem."

The report, which was first issued for consultation in September 2009, sets out 10 recommendations that fall into three categories:

The Committee also recommends that supervisors work closely with their foreign counterparts and relevant resolution authorities to understand how complex group structures and operations could be resolved in a crisis. If an institution's group structures are too complex to permit an orderly and cost-effective resolution, national authorities should consider imposing regulatory incentives, through capital or other prudential requirements, to encourage simplification of the structures.

Al riguardo vi segnalo anche l'articolo di Stefano Micossi su La Voce di qualche giorno fa. Un rapporto più lungo centrato sulla situazione europea è disponibile a questo link: ecco una sintesi delle raccomandazioni del rapporto.

SUMMARY OF RECOMMENDATIONS

All EU cross-border banking groups would be required to sign up to a new deposit guarantee scheme managed by the European Banking Authority (EBA). The scheme would be fully funded ex-ante by levying fees determined on an actuarial risk basis. Participating banks would undertake to provide all relevant information required for effective supervision to the EBA and the Colleges of supervisors.

All banking groups would be supervised and, in case of need,

subjected to mandatory resolution procedures on a consolidated basis,

under the law of the parent company. Subsidiaries chartered in separate

jurisdictions, but unable to survive a crisis of the parent company on their

own, would also fall under the same authority.

Banking groups would be free to set up fully stand-alone

subsidiaries, under the law of the host countries, but the entities would

then have to meet precise requirements of independence of capital,

liquidity and other critical functions.

All national supervisors would have administrative powers to

manage early corrective action and resolution, according to the principles

outlined by the Basel Supervisors.

Supervision, early action and reorganisation would be managed by

strengthened Colleges of supervisors, under the leadership of the parent

company supervisor and a regime of full exchange of information amongst

interested national supervisors. The Colleges of supervisors would make

their proposals to the EBA, which would sanction them with its own

decisions and would mediate disputes between national supervisors.

By offering all interested parties in a resolution procedure the full

guarantee that they will be heard and treated fairly before an independent

authority, the EBA would create the conditions in which jurisdictions other

than that of the parent company will be ready to accept delegating to the

latter the resolution of the entire banking group on a consolidated basis.

Mandated action will also ensure that supervisory forbearance would not

be used to favour national interests to the detriment of stakeholders from

other jurisdictions.

Qui invece trovate gli articoli che il WSJ sta dedicando alla crisi greca.

Eccellente articolo di Thomas Friedman sul New York Times: riassume bene una delle ragioni per cui ammiro gli USA e per cui continuo ad essere un acceso sostenitore dell'ecologia dei cervelli (la necessità di costruire un habitat sociale ed economico che coltivi le idee innovative e le persone creative, indipendentemente da ogni altra loro caratteristica) mentre non sopporto la retorica del ritorno dei cervelli (se li fai tornare per farli rimbecillire a che serve farli rientrare?). Certo che gli USA devono curare alcuni dei loro (e non solo loro) mali se desiderano restare il paese di riferimento per libertà di iniziativa e innovazione: l'Op-Ed di Frank Rich sul Times di oggi sviluppa alcuni spunti di riflessione.

Intanto che l'America riflette su come migliorarsi,

l'Economist dedica un'analisi alla crescita della produttività negli USA, al cui confronto l'Europa impallidisce. Vorrei attirare la vostra attenzione sul confronto tra il tasso di crescita annuale della produttività negli USA e in Italia nel decennio 1998-2008: 2.2% vs. 0.4%. In un decennio questo porta ad una differenza del 20% A me sembra un dato significativo. Anche le previsioni per i prossimi 10 anni, nei quali la produttività USA dovrebbe crescere solo dell'1.5%, contro lo 0.5% italico, sono disarmanti.

l'Economist dedica un'analisi alla crescita della produttività negli USA, al cui confronto l'Europa impallidisce. Vorrei attirare la vostra attenzione sul confronto tra il tasso di crescita annuale della produttività negli USA e in Italia nel decennio 1998-2008: 2.2% vs. 0.4%. In un decennio questo porta ad una differenza del 20% A me sembra un dato significativo. Anche le previsioni per i prossimi 10 anni, nei quali la produttività USA dovrebbe crescere solo dell'1.5%, contro lo 0.5% italico, sono disarmanti.Dopo due decenni così basteranno tre lavoratori USA per produrre lo stesso output orario di quattro lavoratori italiani.

Sul tema della riforma delle banche e della regolamentazione il punto di vista della Fed e della amministrazione Obama sembrano avvicinarsi

mentre sembra chiara l'intenzione del comitato di Basilea di evitare un ripetersi dei bailouts del 2008:

the final report of the Cross-Border Bank Resolution Group of the Basel Committee called for “firm-specific contingency planning” that would help the most interconnected financial companies survive a crisis or, if necessary, be dismantled in an orderly fashion, without risking a global financial crisis.

Il rapporto completo è disponibile a questo link ed ecco il comunicato stampa che lo annuncia:

The Basel Committee on Banking Supervision today issued its final Report and Recommendations of the Cross-border Bank Resolution Group.

Mr Nout Wellink, Chairman of the Basel Committee and President of the Netherlands Bank, noted that "the resolution of a cross-border bank is a complex and multidimensional process and the financial crisis exposed gaps in intervention techniques and tools needed for an orderly resolution. Based on the lessons of the crisis and our analysis of national resolution frameworks, I believe that implementation of the Committee's recommendations will help make meaningful progress toward addressing systemic risk and the too-big-to-fail problem."

The report, which was first issued for consultation in September 2009, sets out 10 recommendations that fall into three categories:

- Strengthening national resolution powers and their cross-border implementation. National authorities need to have powers to intervene sufficiently early and to ensure the continuity of critical functions.

- Firm-specific contingency planning. Banks, as well as key home and host authorities, should develop practical and credible plans to promote resiliency in periods of severe financial distress and to facilitate a rapid resolution should that be necessary. The plans should ensure access to relevant information in a crisis and assist the authorities' evaluation of resolution options. One of the main lessons from the crisis was that the enormous complexity of corporate structure makes resolutions difficult, costly and unpredictable.

- Reducing contagion. Risk mitigation through mechanisms such as netting arrangements, collateralisation practices and the use of regulated central counterparties should be strengthened to limit the market impact of a bank failure.

The Committee also recommends that supervisors work closely with their foreign counterparts and relevant resolution authorities to understand how complex group structures and operations could be resolved in a crisis. If an institution's group structures are too complex to permit an orderly and cost-effective resolution, national authorities should consider imposing regulatory incentives, through capital or other prudential requirements, to encourage simplification of the structures.

Al riguardo vi segnalo anche l'articolo di Stefano Micossi su La Voce di qualche giorno fa. Un rapporto più lungo centrato sulla situazione europea è disponibile a questo link: ecco una sintesi delle raccomandazioni del rapporto.

SUMMARY OF RECOMMENDATIONS

All EU cross-border banking groups would be required to sign up to a new deposit guarantee scheme managed by the European Banking Authority (EBA). The scheme would be fully funded ex-ante by levying fees determined on an actuarial risk basis. Participating banks would undertake to provide all relevant information required for effective supervision to the EBA and the Colleges of supervisors.

All banking groups would be supervised and, in case of need,

subjected to mandatory resolution procedures on a consolidated basis,

under the law of the parent company. Subsidiaries chartered in separate

jurisdictions, but unable to survive a crisis of the parent company on their

own, would also fall under the same authority.

Banking groups would be free to set up fully stand-alone

subsidiaries, under the law of the host countries, but the entities would

then have to meet precise requirements of independence of capital,

liquidity and other critical functions.

All national supervisors would have administrative powers to

manage early corrective action and resolution, according to the principles

outlined by the Basel Supervisors.

Supervision, early action and reorganisation would be managed by

strengthened Colleges of supervisors, under the leadership of the parent

company supervisor and a regime of full exchange of information amongst

interested national supervisors. The Colleges of supervisors would make

their proposals to the EBA, which would sanction them with its own

decisions and would mediate disputes between national supervisors.

By offering all interested parties in a resolution procedure the full

guarantee that they will be heard and treated fairly before an independent

authority, the EBA would create the conditions in which jurisdictions other

than that of the parent company will be ready to accept delegating to the

latter the resolution of the entire banking group on a consolidated basis.

Mandated action will also ensure that supervisory forbearance would not

be used to favour national interests to the detriment of stakeholders from

other jurisdictions.

domenica 21 marzo 2010

Greenspan e la bolla...5 anni (e una grande contrazione) dopo. Speculare sulle valute?

Il New York Times dedica una riflessione a un lungo articolo di Alan Greenspan sulle origini della crisi. Greenspan sembra essere d'accordo sul fatto che per prevenire le crisi future occorre aumentare i requisiti di capitale e liquidità per le banche. Scrive il TImes:

Mr. Greenspan, once celebrated as the “maestro” of economic policy, has seen his reputation dim after failing to avert the credit bubble that nearly brought down the financial system. Now (...) he is calling for a degree of greater banking regulation in several areas.(...)

He argues that regulators should enforce collateral and capital requirements, limit or ban certain kinds of concentrated bank lending, and even compel financial companies to develop “living wills” that specify how they are to be liquidated in an orderly way.

“For years the Federal Reserve had been concerned about the ever-larger size of our financial institutions,” Mr. Greenspan wrote. Fed research has not been able to find economies of scale as banks grow beyond a modest size, he said, and in a 1999 speech, Mr. Greenspan warned that “megabanks” formed through mergers created the potential for “unusually large systemic risks” should they fail.

Mr. Greenspan added: “Regrettably, we did little to address the problem.”

The former Fed chairman also acknowledged that the central bank failed to grasp the magnitude of the housing bubble but argued, as he has before, that its policy of low interest rates was not to blame. He stood by his conviction that little could be done to identify a bubble before it burst, much less to pop it.(...)

In addition to endorsing higher capital and liquidity requirements, Mr. Greenspan said banks and possibly all financial intermediaries should be required to hold bonds that automatically convert to equity when capital falls below a certain threshold. That could help reduce the “moral hazard” that exists because the banks that failed did not suffer the full costs of their actions.

The Senate is contemplating a mechanism by which the government can seize and dismantle a huge, interconnected financial company before panic spreads.

For a big, interconnected company, regulators should initiate a special bankruptcy process, he wrote. A bankruptcy judge would require creditors to take a haircut before the company is reorganized. The company should then be split up into separate units, “none of which should be of a size that is too big to fail,” Mr. Greenspan wrote.

Nell'ultimo numero dell'Economist viene aggiornato il Big Mac index, che misura il potere d'acquisto relativo delle diverse valute mendiante il prezzo del Big Mac: l'euro risulta ancora sopravvalutato del 25% rispetto al dollaro, ma gli estremi spettano alla corona norvegese (sopravvalutata del 90%)

e allo yuan (sottovalutato del 50%)...Scommettere contro la corona norvegese è facile (ad esempio lo permette la mia banca, Fineco). Mi pare invece più complicato scommettere sulla rivalutazione dello yuan: qualcuno conosce un modo?

Mr. Greenspan, once celebrated as the “maestro” of economic policy, has seen his reputation dim after failing to avert the credit bubble that nearly brought down the financial system. Now (...) he is calling for a degree of greater banking regulation in several areas.(...)

He argues that regulators should enforce collateral and capital requirements, limit or ban certain kinds of concentrated bank lending, and even compel financial companies to develop “living wills” that specify how they are to be liquidated in an orderly way.

“For years the Federal Reserve had been concerned about the ever-larger size of our financial institutions,” Mr. Greenspan wrote. Fed research has not been able to find economies of scale as banks grow beyond a modest size, he said, and in a 1999 speech, Mr. Greenspan warned that “megabanks” formed through mergers created the potential for “unusually large systemic risks” should they fail.

Mr. Greenspan added: “Regrettably, we did little to address the problem.”

The former Fed chairman also acknowledged that the central bank failed to grasp the magnitude of the housing bubble but argued, as he has before, that its policy of low interest rates was not to blame. He stood by his conviction that little could be done to identify a bubble before it burst, much less to pop it.(...)

In addition to endorsing higher capital and liquidity requirements, Mr. Greenspan said banks and possibly all financial intermediaries should be required to hold bonds that automatically convert to equity when capital falls below a certain threshold. That could help reduce the “moral hazard” that exists because the banks that failed did not suffer the full costs of their actions.

The Senate is contemplating a mechanism by which the government can seize and dismantle a huge, interconnected financial company before panic spreads.

For a big, interconnected company, regulators should initiate a special bankruptcy process, he wrote. A bankruptcy judge would require creditors to take a haircut before the company is reorganized. The company should then be split up into separate units, “none of which should be of a size that is too big to fail,” Mr. Greenspan wrote.

Nell'ultimo numero dell'Economist viene aggiornato il Big Mac index, che misura il potere d'acquisto relativo delle diverse valute mendiante il prezzo del Big Mac: l'euro risulta ancora sopravvalutato del 25% rispetto al dollaro, ma gli estremi spettano alla corona norvegese (sopravvalutata del 90%)

e allo yuan (sottovalutato del 50%)...Scommettere contro la corona norvegese è facile (ad esempio lo permette la mia banca, Fineco). Mi pare invece più complicato scommettere sulla rivalutazione dello yuan: qualcuno conosce un modo?

sabato 20 marzo 2010

Il consumatore spiato? Aggiornamento al 19 marzo 2010.

Fate attenzione quando andate a fare la spesa al supermercato: vi potrebbero stare spiando...ecco quanto racconta il New York Times di oggi:

The curvy mannequin piqued the interest of a couple of lanky teenage boys. Little did they know that as they groped its tight maroon shirt in the clothing store that day, video cameras were rolling.

At a mall, a father emerged from a store dragging his unruly young son by the scruff of the neck, as if he were the family cat. The man had no idea his parenting skills were being immortalized.

At an office supply store, a mother decided to get an item from a high shelf by balancing her small child on her shoulders, unaware that she, too, was being recorded.

These scenes may seem like random shopping bloopers, but they are meaningful to stores that are striving to engineer a better experience for the consumer, and ultimately, higher sales for themselves. Such clips, retailers say, can help them find solutions to problems in their stores — by installing seating and activity areas to mollify children, for instance, or by lowering shelves so merchandise is within easy reach.

Qui trovate alcune riprese che immortalano i consumatori in momenti più o meno imbarazzanti...

Il Financial Times si interroga sul significato dei nuovi minimi dell'indice di volatilità VIX:

Mr Curnutt says that the benefit of the fall in the Vix is that investors can buy insurance against a decline in shares much more cheaply, a strategy which many investors continue to pursue. Indeed, there has been some pick-up in hedging activities, as some investors see a sharp fall of the Vix as a potential sign of turbulence ahead, a type of contrarian indicator.

The analysis by Birinyi Associates found that this had, on occasion, proved to be the right strategy. “It [the Vix] might, however, be useful in that it appears that high volatility might actually be a contrarian indicator,” the study said.

Whether low volatility has the same contrarian value is less clear-cut. The coming months will offer more valuable market history to analyse.

Sempre il Financial Times attribuisce al ritorno della risk-aversion il ritracciamento di ieri della borsa...

...mentre qui potere leggere (e qui potete vedere un breve video) dell'avventura di un signore che di avversione per il rischio proprio non ne ha...

Per i comuni mortali... l'unico investimento privo di rischio è tradizionalmente costituito dai buoni del Tesoro USA...ma anche questa possibilità potrebbe ormai appartenere al passato...:

Moody’s said the United States and other major Western nations, particularly Britain, have moved “substantially” closer to losing their gilt-edged ratings. The ratings are “stable,” but “their ‘distance-to-downgrade’ has in all cases substantially diminished,” the credit ratings agency said. (...)

“Growth alone will not resolve an increasingly complicated debt equation,” Moody’s said. “Preserving debt affordability” — the ratio of interest payments to government revenue — “at levels consistent with Aaa ratings will invariably require fiscal adjustments of a magnitude that, in some cases, will test social cohesion.” The United States, Britain, France and Germany have always been rated triple-A by Moody’s, with the United States first rated in 1949.

“Growth alone will not resolve an increasingly complicated debt equation,” Moody’s said. “Preserving debt affordability” — the ratio of interest payments to government revenue — “at levels consistent with Aaa ratings will invariably require fiscal adjustments of a magnitude that, in some cases, will test social cohesion.” The United States, Britain, France and Germany have always been rated triple-A by Moody’s, with the United States first rated in 1949.

...proprio mentre sta per abbattersi sul mercato una montagna di debito corporate in scadenza:

When the Mayans envisioned the world coming to an end in 2012 — at least in the Hollywood telling — they didn’t count junk bonds among the perils that would lead to worldwide disaster.

Maybe they should have, because 2012 also is the beginning of a three-year period in which more than $700 billion in risky, high-yield corporate debt begins to come due, an extraordinary surge that some analysts fear could overload the debt markets.

With huge bills about to hit corporations and the federal government around the same time, the worry is that some companies will have trouble getting new loans, spurring defaults and a wave of bankruptcies.

The United States government alone will need to borrow nearly $2 trillion in 2012, to bridge the projected budget deficit for that year and to refinance existing debt.(...)

The result is a potential financial doomsday, or what bond analysts call a maturity wall. From $21 billion due this year, junk bonds are set to mature at a rate of $155 billion in 2012, $212 billion in 2013 and $338 billion in 2014.

The credit markets have gradually returned to normal since the financial crisis, particularly in recent months, making more loans available to companies and signaling confidence in the pace of economic recovery. But the issue is whether they can absorb the coming surge in demand for credit.

Ecco l'aggiornamento al 19 marzo 2010

The curvy mannequin piqued the interest of a couple of lanky teenage boys. Little did they know that as they groped its tight maroon shirt in the clothing store that day, video cameras were rolling.

At a mall, a father emerged from a store dragging his unruly young son by the scruff of the neck, as if he were the family cat. The man had no idea his parenting skills were being immortalized.

At an office supply store, a mother decided to get an item from a high shelf by balancing her small child on her shoulders, unaware that she, too, was being recorded.

These scenes may seem like random shopping bloopers, but they are meaningful to stores that are striving to engineer a better experience for the consumer, and ultimately, higher sales for themselves. Such clips, retailers say, can help them find solutions to problems in their stores — by installing seating and activity areas to mollify children, for instance, or by lowering shelves so merchandise is within easy reach.

Qui trovate alcune riprese che immortalano i consumatori in momenti più o meno imbarazzanti...

Il Financial Times si interroga sul significato dei nuovi minimi dell'indice di volatilità VIX:

Mr Curnutt says that the benefit of the fall in the Vix is that investors can buy insurance against a decline in shares much more cheaply, a strategy which many investors continue to pursue. Indeed, there has been some pick-up in hedging activities, as some investors see a sharp fall of the Vix as a potential sign of turbulence ahead, a type of contrarian indicator.

The analysis by Birinyi Associates found that this had, on occasion, proved to be the right strategy. “It [the Vix] might, however, be useful in that it appears that high volatility might actually be a contrarian indicator,” the study said.

Whether low volatility has the same contrarian value is less clear-cut. The coming months will offer more valuable market history to analyse.

Sempre il Financial Times attribuisce al ritorno della risk-aversion il ritracciamento di ieri della borsa...

...mentre qui potere leggere (e qui potete vedere un breve video) dell'avventura di un signore che di avversione per il rischio proprio non ne ha...

Per i comuni mortali... l'unico investimento privo di rischio è tradizionalmente costituito dai buoni del Tesoro USA...ma anche questa possibilità potrebbe ormai appartenere al passato...:

Moody’s said the United States and other major Western nations, particularly Britain, have moved “substantially” closer to losing their gilt-edged ratings. The ratings are “stable,” but “their ‘distance-to-downgrade’ has in all cases substantially diminished,” the credit ratings agency said. (...)

“Growth alone will not resolve an increasingly complicated debt equation,” Moody’s said. “Preserving debt affordability” — the ratio of interest payments to government revenue — “at levels consistent with Aaa ratings will invariably require fiscal adjustments of a magnitude that, in some cases, will test social cohesion.” The United States, Britain, France and Germany have always been rated triple-A by Moody’s, with the United States first rated in 1949.

“Growth alone will not resolve an increasingly complicated debt equation,” Moody’s said. “Preserving debt affordability” — the ratio of interest payments to government revenue — “at levels consistent with Aaa ratings will invariably require fiscal adjustments of a magnitude that, in some cases, will test social cohesion.” The United States, Britain, France and Germany have always been rated triple-A by Moody’s, with the United States first rated in 1949....proprio mentre sta per abbattersi sul mercato una montagna di debito corporate in scadenza:

When the Mayans envisioned the world coming to an end in 2012 — at least in the Hollywood telling — they didn’t count junk bonds among the perils that would lead to worldwide disaster.

With huge bills about to hit corporations and the federal government around the same time, the worry is that some companies will have trouble getting new loans, spurring defaults and a wave of bankruptcies.

The United States government alone will need to borrow nearly $2 trillion in 2012, to bridge the projected budget deficit for that year and to refinance existing debt.(...)

The result is a potential financial doomsday, or what bond analysts call a maturity wall. From $21 billion due this year, junk bonds are set to mature at a rate of $155 billion in 2012, $212 billion in 2013 and $338 billion in 2014.