A slew of poor economic data over the past two weeks suggests that the U.S. economy is headed for a U-shaped recovery—at best—in 2010. The macro news, (...) actually suggests a significant downside risk (...). The U.S. faces continued challenges in H2—particularly as historic levels of fiscal stimulus fade—and appears far too close to the tipping point of a double-dip recession.

This is not the conventional wisdom. Heated debate continues to rage in the United States on whether the economic recovery will be V-shaped (with a rapid return to robust growth above potential), U-shaped (slow anemic, sub-par, below trend growth for at least the next two years) or W-shaped (a double-dip recession). The V camp includes distinguished research groups and individuals such as Ed Hyman’s ISI, Larry Meyer’s Macroeconomic Advisors, the research group of JP Morgan, Michael Mussa and others. The U camp includes—among others—Roubini Global Economics, Goldman Sachs’ U.S. economic research group, PIMCO and Ken Rogoff. As early as August 2009, I worried in a Financial Times op-ed about the risk of a double-dip recession even if our RGE benchmark scenario characterizes the risk of a W as still a low probability event (20% probability) as opposed to a 60% probability for a U-shaped recovery. Others concerned about the double-dip risk include also David Rosenberg, Gary Shilling and John Makin.

Ed Hyman and I debated whether the recovery would be U or V-shaped on a February 22 conference call attended by over 2,200 listeners. Since that call, a slew of new U.S. macro data have come out. They have been almost uniformly poor, if not outright awful. (...)

The eurozone (EZ) debt crisis, which RGE discusses in depth in a major new paper, predisposes Europe to a rising double-dip risk, due to the wave of fiscal austerity sweeping the periphery of the EZ. Even if the EZ doesn’t enter a double dip, the growth of domestic demand there will be as or more constrained than in the United States. This, in turn, will be a drag on the potential for U.S. export growth. The U.S. dollar rally on risk aversion reflects this risk. (...) A similar retrenchment may well lie ahead in the United Kingdom, given rising fiscal sustainability concerns and the threat of a sterling crisis. Europe then will have great difficulty being a source of demand for U.S. exports, and may even provide impetus to faltering global demand growth, contributing to the threat of a wider double dip across high-income countries.

Ho trovato interessante questo post di Bespoke sulle nanotecnologie:

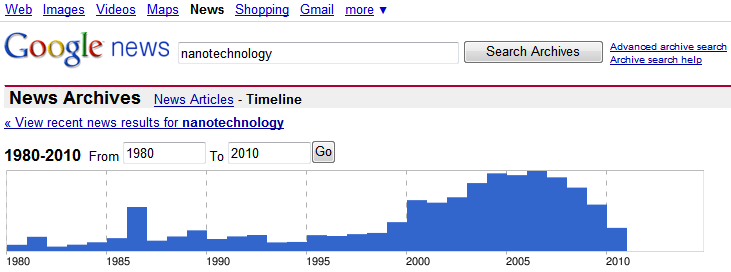

Back in the "good 'ole days" of the mid-2000s, investors were riding a bull market wave and looking for "the next big thing." One of those "next big things" was nanotechnology. Ever since the collapse began in 2007, however, the nanotech craze seems all but forgotten. We can't remember the last time we read or watched something about nanotech. A search of the term on Google News Archives confirms that there has indeed been a decline in nanotech coverage. As shown below, news articles containing the word "nanotechnology" peaked in 2006, and they've been declining steadily ever since. (Interestingly, this year does seem to be on pace to eclipse 2009.)

click to enlarge

Stocks and ETFs relating to nanotech have also lost investor interest. The PowerShares Nanotech ETF (PXN) actually came out right when the nanotech craze was peaking in 2005. As shown below, the ETF never really went anywhere. Even as the overall market was rising from 2005 to late 2007, PXN traded sideways. When the collapse hit, PXN wasn't spared.

Un'occasione per investitori contrarian? .

Tra gli investitori contrarian spicca Michael Burry, un giovane value investor di grande successo: Vanity Fair gli dedica un lungo articolo molto ben scritto che vi raccomando caldamente di leggere.

Nessun commento:

Posta un commento