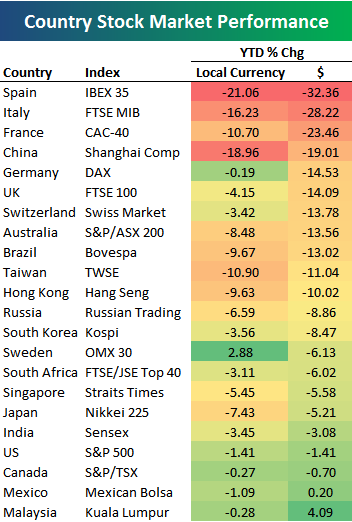

First, the euro zone needs to approve the €750 billion ($927 billion) bail-out package agreed three weeks ago. Second, individual countries must press ahead with austerity packages and, equally important, initiate the labor-market reforms vital to improving competitiveness. Finally, the European Union should commit to a full stress-test of its banking system and, where necessary, commit to further recapitalizations, as U.S. Treasury Secretary Timothy Geithner recommended this week. That might just bring U.S. investors back on board.

Intanto sul New York Times di oggi si discute sul rischio che l'Europa finisca in deflazione:

(...) some economists say it has become a driving obsession that has blinded the bank to a potentially bigger threat to Europe: deflation.

The central bank’s doubters grew louder after it made a big show of taking measures to cancel out the supposed inflationary impact of the government bond purchases it began on May 10 to help keep Greece and several other euro zone countries from defaulting on their debts.

“It’s nuts: how can they be concerned about the inflationary impact of this?” said Carl B. Weinberg, chief economist of High Frequency Economics in Valhalla, N.Y. “If I were the head of the E.C.B., I would be printing money to avert the decline in the money supply.”

Many economists regard deflation as more dangerous than inflation, because it prompts consumers to delay purchases as they wait for lower prices, creating a downward spiral of lower demand and production. Deflation is also bad for debtors like Greece, because they may have to pay back money that would be worth more than it was when they borrowed it.

Economists like Mr. Weinberg — and a few policy makers as well — are beginning to worry that a danger of deflation in Europe, similar to the one that strangled Japanese growth for most of the 1990s, is a bigger threat than inflation.

Prices fell in Ireland in April, while inflation was below 1 percent in five other euro zone countries. The problem also extends outside the euro zone.

“We all share some risks and problems in common with Japan circa 1995,” Adam S. Posen, a member of the Bank of England’s monetary policy committee, told an audience at the London School of Economics on May 2.

The United States is also at risk, Mr. Posen said, though he rated the chances of deflation there as low. But just as Japan did in the 1990s, the European Central Bank and the United States Federal Reserve have cut interest rates close to zero while pumping huge amounts of credit into their economies. That means the two central banks would have limited policy tools left with which to combat a collapse in prices and demand.

The downward pressure on prices has its roots in the economic decline that followed the 2008 financial crisis, but Europe’s sovereign debt problems are likely to add extra impetus. Governments, including those of Spain and Germany, are sharply reducing spending to lower their deficits, which will inevitably curb consumer demand and employment, hindering growth.(...)

Spanish core inflation already turned negative in April.

A mild decline in prices in a few euro zone countries can be managed, economists say, but it will add to the risks of deflation. And the central bank will face more difficulty than usual in devising a monetary policy that fits both the ailing countries and the faster-growing economies like Germany and France.(...)

The recent decline of the euro against the dollar could create some inflation. Oil and other commodities are priced in dollars and could become more expensive in euros.

Still, few economists see prices rising. “There is no reason to fear high inflation for the time being,” Simon Junker, a Commerzbank analyst, said in a note.

Vi segnalo tre post di Brad De Long:

- Come prevedere i rendimenti futuri delle azioni USA? La conclusione è moderatamente ottimista: It's hard to see there being a large, permanent wedge between average real stock returns on the one hand and average earnings yields on the other. With trend earnings on the DJIA somewhere around 600 and with Treasury rates as low as they are, it's hard to argue that U.S. stocks will be outperformed by other asset classes over any even moderately long horizon. Vorrei dedicare un post all'argomento appena trovo un po' di tempo.

- La legge di Walras in azione: ma dove sono le obbligazioni sicure?...

- ...e infatti gli investitori a caccia di titoli di alta qualità fanno volare le obbligazioni trentennali del Tesoro USA, con rendimenti ormai appena superiori al 4%. Scrive De Long: In late May, the yield to maturity of the 30-year United States Treasury bond was 4.07% per year – down a full half a percentage point since the start of the month. That means that a 30-year Treasury bond had jumped in price by more than 15%. So a marginal investor was willing to pay more than 15% more cash and more than 30% more equities for US Treasury bonds at the end of the month than at the beginning. This signals a remarkable shift in relative demand for high-quality and liquid financial assets – an extraordinary rise in market-wide excess demand for such assets.

Why does this matter? Because, as economist John Stuart Mill wrote in the first half of the nineteenth century, excess demand for cash (or for some broader range of high-quality and liquid assets) is excess supply of everything else. What economists three generations later were to call Walras’s Law is the principle that any market in which people are planning to buy more than is for sale must be counterbalanced by a market or markets in which people are planning to buy less.We have seen this principle in action since the early fall of 2007, as growing excess demand for safe, liquid, high-quality financial assets has carried with it growing excess supply for the goods and services that are the products of ongoing human labor. This is true to such an extent that there is now a 10% gap between the global economy’s current output and what it would be producing if it were in its normal relatively healthy state of near-balance.And global financial markets are now telling us that this excess demand for safe, liquid, high-quality financial assets has just gotten bigger.To some small degree, a change in investor sentiment has induced the rise in excess demand for such assets. After all, we can assume that the animal spirits of investors and financiers has been further depressed as a psychological reaction to the exuberant belief just a few years ago in the powers of financial engineering.But most of the recent shift has come not from an increase in demand for safe, liquid, high-quality financial assets, but from a decrease in supply: six months ago, bonds issued by the governments of southern Europe were regarded as among the high-quality assets in the world economy that one could safely and securely hold; now they are not.

Why does this matter? Because, as economist John Stuart Mill wrote in the first half of the nineteenth century, excess demand for cash (or for some broader range of high-quality and liquid assets) is excess supply of everything else. What economists three generations later were to call Walras’s Law is the principle that any market in which people are planning to buy more than is for sale must be counterbalanced by a market or markets in which people are planning to buy less.We have seen this principle in action since the early fall of 2007, as growing excess demand for safe, liquid, high-quality financial assets has carried with it growing excess supply for the goods and services that are the products of ongoing human labor. This is true to such an extent that there is now a 10% gap between the global economy’s current output and what it would be producing if it were in its normal relatively healthy state of near-balance.And global financial markets are now telling us that this excess demand for safe, liquid, high-quality financial assets has just gotten bigger.To some small degree, a change in investor sentiment has induced the rise in excess demand for such assets. After all, we can assume that the animal spirits of investors and financiers has been further depressed as a psychological reaction to the exuberant belief just a few years ago in the powers of financial engineering.But most of the recent shift has come not from an increase in demand for safe, liquid, high-quality financial assets, but from a decrease in supply: six months ago, bonds issued by the governments of southern Europe were regarded as among the high-quality assets in the world economy that one could safely and securely hold; now they are not.