Economic Memo

Employment Data May Be the Key to the President's Job

By BINYAMIN APPELBAUM

No president since Franklin Roosevelt has won re-election with unemployment above 7.2 percent. To keep his own job, it appears President Obama may have to defy this trend.

Il tema è caro a Paul Krugman che ieri sul suo blog sottolineava ancora una volta il rischio che si ripetano gli errori che nel 1937 fecero ripiombare gli USA in depressione. Secondo Krugman il rischio che ciò si verifichi è molto alto in Europa, se se la prende con Bini Smaghi: The research staff at the NY Fed won’t; but the ECB very probably will, and the Board of Governors is under a lot of political pressure to raise rates.

We’ve learned a lot less these past 74 years than you might have imagined — or rather, we learned some stuff, but have spent the last few decades unlearning it.Update: And here’s Lorenzo Bini Smaghi of the ECB insisting that yes, we do intend to repeat the mistake of 1937.

Se è possibile trovo ancora più allarmante questo post sul blog di Krugman dedicato all'ultimo commento di Martin Wolf sul Financial Times di qualche giorno fa: slow-motion bank runs are already in progress in the European periphery, and that these countries’ banking systems are being sustained only by a process in which, say, Ireland’s central bank borrows from the Bundesbank and then lends the funds on to Irish private banks to replace the fleeing deposits. Here are claims among central banks as of the end of last year:

Financial Times: Claims among European central banks

You can see why we’re now at the panic stage. The Bundesbank is already very upset about its large claims on troubled debtors, which are backed by sovereign debt as collateral. Yet if financing stops in the wake of a debt restructuring, the result will be to collapse the debtor nations’ banking systems, a process Martin believes would lead to their ejection from the euro. (He makes me look like an optimist!)

So the ECB keeps saying that restructuring is unthinkable. Yet austerity programs are not working; the prospect of a return to normal financing is receding rather than approaching.

If you ask me, the water level has now dropped so far that the fuel rods are exposed. We really are in meltdown territory.

Ieri i mercati hanno subito la pressione sia dell'ulteriore downgrade della Grecia che dei pessimi dati macro provenienti dagli U.S.A.: ecco due titoli dal Financial Times di oggi

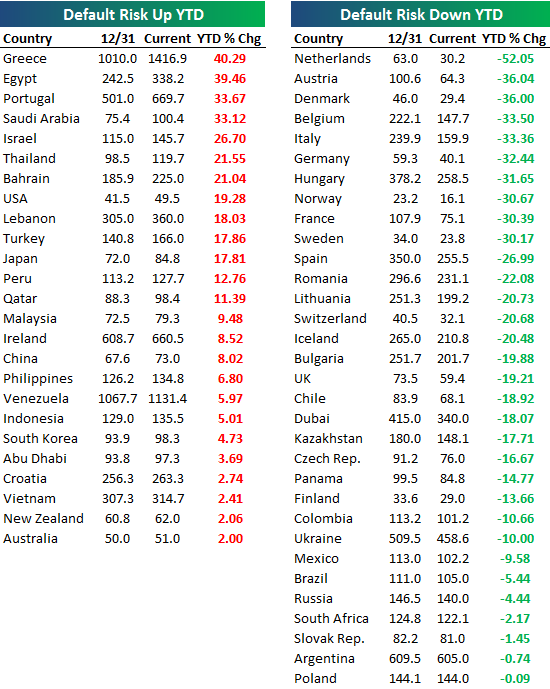

C'è da osservare come il calo dei tassi dei Treasury bonds si accompagna ormai da settimane a un rialzo dei CDS che per il debito USA con scadenza a cinque anni sono ormai vicini a 50 punti base: dall'inizio dell'anno

C'è da osservare come il calo dei tassi dei Treasury bonds si accompagna ormai da settimane a un rialzo dei CDS che per il debito USA con scadenza a cinque anni sono ormai vicini a 50 punti base: dall'inizio dell'annoad oggi l'aumento (in termini relativi) del prezzo dei CDS mette gli U.S.A. davvero in cattiva compagnia, come mostra la tabella qui accanto tratta da seekingalpha.

C'è davvero chi compra obbligazioni del governo U.S.A. e simultaneamente si protegge da rischio default con i CDS? Magari sperando nell'insolvenza "tecnica" se repubblicani e democratici non riesocno a mettersi d'accordo entro il 2 agosto?

Nessun commento:

Posta un commento