ed ecco una mia elaborazione relativa all'indice Stoxx 50, diviso in cinque quintili

secondo la performance tra il febbraio del 2008 e il febbraio del 2009, confrontata con quella nell'anno successivo (conclusosi a fine febbraio 2010): anche in

Europa gli ultimi sono diventati i primi!

Europa gli ultimi sono diventati i primi!

| Società | Performance (28/2/2008-28/2/2009) | Performance Media per quintile (28/2/2008-28/2/2009) | Performance (28/2/2009-28/2/2010) | Performance Media per quintile (28/2/2009-28/2/2010) |

| ROYAL BANK OF SCOTLAND GRP | -92,80% | -75,12% | 65,48% | 113,29% |

| ING GRP | -83,52% | 133,21% | ||

| BARCLAYS | -79,90% | 234,58% | ||

| UNICREDIT | -79,32% | 127,53% | ||

| DEUTSCHE BANK | -72,02% | 124,42% | ||

| ARCELORMITTAL | -69,51% | 81,04% | ||

| ANGLO AMERICAN | -69,05% | 138,76% | ||

| NOKIA | -68,80% | 31,58% | ||

| RIO TINTO | -68,51% | 126,10% | ||

| DAIMLER | -67,72% | 70,24% | ||

| AXA | -67,36% | -58,81% | 106,24% | 66,86% |

| GRP SOCIETE GENERALE | -64,90% | 70,81% | ||

| UBS | -63,81% | 33,91% | ||

| ASSICURAZIONI GENERALI | -58,13% | 39,77% | ||

| BCO BILBAO VIZCAYA ARGENTARIA | -57,92% | 64,94% | ||

| INTESA SANPAOLO | -56,49% | 33,39% | ||

| BNP PARIBAS | -56,37% | 110,34% | ||

| BCO SANTANDER | -55,95% | 94,88% | ||

| ALLIANZ | -54,36% | 58,12% | ||

| SIEMENS | -52,79% | 56,19% | ||

| PHILIPS ELECTRONICS | -50,98% | -42,15% | 68,59% | 51,26% |

| E.ON | -50,70% | 28,15% | ||

| BASF | -47,70% | 87,80% | ||

| IBERDROLA | -45,83% | 13,73% | ||

| ABB | -45,37% | 55,98% | ||

| CREDIT SUISSE GRP | -44,38% | 64,94% | ||

| HSBC | -35,87% | 68,09% | ||

| ROCHE HLDG P | -35,09% | 34,89% | ||

| GDF SUEZ | -33,41% | 8,99% | ||

| BHP BILLITON | -32,15% | 81,46% | ||

| ENI | -30,80% | -24,79% | 4,48% | 20,00% |

| ROYAL DUTCH SHELL A | -26,66% | 15,09% | ||

| UNILEVER NV | -25,72% | 44,92% | ||

| BAYER | -25,11% | 27,81% | ||

| TOTAL | -25,03% | 9,34% | ||

| DEUTSCHE TELEKOM | -23,91% | -1,20% | ||

| TELEFONICA | -23,54% | 17,23% | ||

| NESTLE | -23,24% | 39,41% | ||

| VODAFONE GRP | -23,05% | 12,98% | ||

| DIAGEO | -20,79% | 29,91% | ||

| FRANCE TELECOM | -20,06% | -8,50% | -3,28% | 21,27% |

| SAP | -19,28% | 28,40% | ||

| BP | -17,90% | 29,10% | ||

| NOVARTIS | -17,05% | 40,00% | ||

| TESCO | -16,80% | 25,96% | ||

| SANOFI-AVENTIS | -16,14% | 31,30% | ||

| BRITISH AMERICAN TOBACCO | -5,17% | 24,07% | ||

| GLAXOSMITHKLINE | -2,99% | 13,56% | ||

| ERICSSON LM B | 11,94% | -4,93% | ||

| ASTRAZENECA | 18,49% | 28,56% | ||

| DJ STOXX 50 | -44,48% | 39,53% | ||

| DJ STOXX 600 | -45,78% | 42,15% |

Se davvero il futuro dell'auto è elettrico, e se non si trovano soluzioni migliori, il mercato delle batterie agli ioni di litio potrebbe esplodere, offrendo a investitori tempestivi e coraggiosi interessanti opportunità di profitto. Questa è in estrema sintesi, la tesi bullish di chi suggerisce di investire in litio. Ne parla il New York Times di qualche giorno fa che tuttavia osserva come:

By the standards of traditional gold and copper booms, the increase in interest in lithium is still muted among big mining companies. Supplies of lithium are plentiful for now, and the price of lithium chemicals actually declined at the end of last year because of the economic slowdown. The price for lithium carbonate, the basic lithium compound used in batteries, had been around $5,000 a ton for the last five years or so, and has leveled at about $4,000 since October.

Ho trovato divertente il post di Pablo Triana su Willmott

che vi propongo insieme alla canzone di Marvin Gaye alla quale si ispira

Heard through the media grapevine after 1997 Asian crisis and 1998 LTCM crisis (which almost destroyed the system):

"The answer is not to reject quantitative finance but to be honest about its limitations. Models have their places but they must be coupled with more subjective approaches to risk, such as stress tests and scenario-planning"

Heard through the media grapevine after 2008 credit crisis (which destroyed the system and almost caused a global depression):

"The answer is not to reject quantitative finance but to be honest about its limitations. Models have their places but they must be coupled with more subjective approaches to risk, such as stress tests and scenario-planning"

To be heard through the grapevine after 2015 sovereign debt CDO crisis (which would do away with the euro, result in the acquisition of Greece by private equity funds, and force President Palin to expulse California from the Union):

"The answer is not to reject quantitative finance but to be honest about its limitations. Models have their places but they must be coupled with more subjective approaches to risk, such as stress tests and scenario-planning"

E se al soul e al rhythm and blues preferite il tango vi consiglio la lettura dei due

articoli di Satyajit Das sulla regolamentazione dei derivati che potete trovare su

eurointelligence qui e qui. Con tutta la confusione che stanno facendo i commentatori in questi giorni li troverete davvero chiari e utili per farsi un'opinione. Intanto un po' di ordine sulle cifre del fenomeno.

Il valore totale nozionale del mercato dei derivati nel giugno del 2009 era di circa 605 trilioni di dollari, cioè 605*10^12 US$, pari a circa una decina di volte il GDP mondiale.

Attenzione però: il valore nozionale è dato dal valore complessivo degli asset sottostanti i contratti derivati stipulati. E' dunque utile per avere un'idea della dimensione del fenomeno e serve per farsi un'idea dell'uso sistematico (e a volte parossistico) della leva finanziaria

Secondo Das:

The size of the market is inconsistent with the thesis that derivatives are merely a vehicle for hedging and risk management.

Current regulatory proposals do not attempt to deal with the size of the derivatives markets. The current debate about "too big to fail" banks may indirectly affect the size issue.

Oltre al problema dell'eccesso di leva - con i conseguenti rischi sistemici e di liquidità - un punto fondamentale da tenere presente è che molti prodotti sono troppo complessi e illiquidi per essere "prezzati" efficientemente: è chiaro in questo caso il vantaggio economico per chi li crea mentre la mancanza di trasparenza e di efficienza finisce con il danneggiare l'intero mercato.

La complessità di un derivato comporta anche numerosi problemi legati alla scelta e all'uso dei modelli impiegati per calcolarne il prezzo:

Model based valuations drive pricing of transactions and dealer hedging. They also are used to calculate the risk of the transactions and ultimately to derive the capital required to be held for regulatory and internal purposes.

The model-based valuations are also used to determine earnings and ultimately bonus payments for dealer staff.

Non-professional dealers rarely have the required sophisticated pricing and valuation systems. They are dependent upon valuation date (predominantly) supplied by dealers or (less frequently) rely on pay-as-you-go pricing services.

Investors use the model-based prices to generate values for their fund units. Investors transact at these model-based prices when they invest or redeem investments

The accuracy and tractability of derivative valuation, especially for complex products, is questionable.

Nei contratti derivati ciascuna delle due parti si assume il rischio di credito dell'altra, ovvero il rischio che la controparte sia effettivamente in grado di mantenere fede agli obblighi contrattuali. Il rischio di controparte è al centro delle proposte di riforma finanziaria con la proposta della creazione di una central clearinghouse (CCP) e con un adeguamento dei requisiti di capitale richiesti alle controparti. Non è chiaro tuttavia come affrontare la regolamentazione senza creare altri rischi, sia di concentrazione che di liquidità:

Current regulatory proposals do not address liquidity risks in derivative markets. Interestingly, the CCP may inadvertently increase liquidity risk as more participants may be subject to margining and unexpected demands on cash resources. The BIS has proposed an extensive regime of liquidity risk management controls that would, in part, cover some liquidity risks.

La questione della regolamentazione dei derivati è molto complessa, tecnica e di poca utilità se non si riesce a ottenere un coordinamento internazionale. Così Das chiude il suo secondo articolo:

There will be a familiar threat. Lack of international agreement and regulatory uniformity makes compliance impractical. Banks and derivative activity will relocate with losses of jobs and taxes to the host country. Familiar arguments will be heard regarding the loss of competitive advantage, diminished financial innovation, slower capital formation and higher cost of capital. Each is a well-known step in the familiar "regulatory tango".The complexity of the issues means that ultimately no laws may be truly effective. As one famous law maker, Adlai Stevenson, observed "Laws are never as effective as habits."

There will be a familiar threat. Lack of international agreement and regulatory uniformity makes compliance impractical. Banks and derivative activity will relocate with losses of jobs and taxes to the host country. Familiar arguments will be heard regarding the loss of competitive advantage, diminished financial innovation, slower capital formation and higher cost of capital. Each is a well-known step in the familiar "regulatory tango".The complexity of the issues means that ultimately no laws may be truly effective. As one famous law maker, Adlai Stevenson, observed "Laws are never as effective as habits."Groucho Marx observed that "[government] is the art of looking for trouble, finding it, misdiagnosing it and then misapplying the wrong remedies." Legislators and regulators are likely to discover the truth of that proposition in their attempts to regulate the derivative market.

3 commenti:

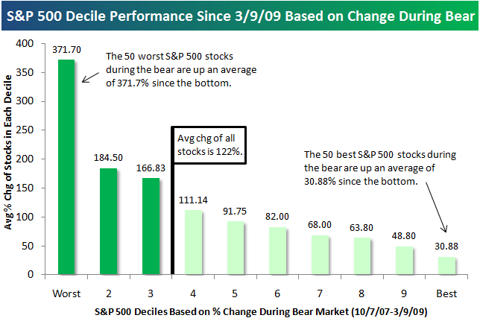

Ciao Stefano. Più che i dati mediani sui gruppi di best e worst performers - sarebbe bello avere queste statistiche prima degli eventi, in modo da poter uscire ed entrare nei tempi giusti e sulle azioni giuste! - e' interessante vedere i nomi dei worst performers (banche e aziende che hanno usato pesantemente la leva finanziaria per m&a) e i best performers (vari pharma, retail intelligenti e ... il vizio !).

Riguardo al litio, periodicamente un imbonitore mi manda una email (chi gli avrà dato il mio indirizzo boh) per invitarmi a investire in 'tremendous opportunities' su azioni OTC di lithium mining companies. Richiesta che invariabilmente interpreto come segnale negativo ...

Caro Antonio, sono d'accordo che "sarebbe bello avere queste statistiche prima degli eventi" ma....

...credi che se conoscessi il futuro perderei tempo a scrivere un blog?

Scherzi a parte,

c'è un famoso esempio del premio Nobel Robert Merton che dimostra il valore di 1 bit di informazione (ben scelto) proveniente dal futuro al mese: sapendo in anticipo ogni mese se l'indice SP500 avrà un rendimento migliore delle obbligazioni, ed investendo di conseguenza, nel periodo 1927-1978 invece di ottenere un rendimento dalle azioni dell'8.5% annuo si ottiene uno spettacolare 35% (praticamente senza drawdowns)...

La prossima volta che ti scrive un imbonitore puoi provare a proporgli questo tipo di strategia!

Posta un commento