Alla fine il prelievo sui depositi bancari a Cipro si è limitato a quelli oltre i 100mila euro...un prelievo del 37,5%...Le banche hanno riaperto giovedì, il governo ha imposto restrizioni di capitale, e la favola dell'unione monetaria ha subito un ennesimo duro colpo. Certo, Cipro è piccola. Sarà comunque interessante vedere come reagirà l'isola con una contrazione del GDP del 20% in soli 12 mesi e con la disoccupazione che esplode. Di fronte ai grandi del mondo (FMI) e dell'Europa (CE e BCE) ai ciprioti rimane la percezione di immaterialità.

Alla fine il prelievo sui depositi bancari a Cipro si è limitato a quelli oltre i 100mila euro...un prelievo del 37,5%...Le banche hanno riaperto giovedì, il governo ha imposto restrizioni di capitale, e la favola dell'unione monetaria ha subito un ennesimo duro colpo. Certo, Cipro è piccola. Sarà comunque interessante vedere come reagirà l'isola con una contrazione del GDP del 20% in soli 12 mesi e con la disoccupazione che esplode. Di fronte ai grandi del mondo (FMI) e dell'Europa (CE e BCE) ai ciprioti rimane la percezione di immaterialità.Noi possiamo stare tranquilli: l'Italia non è Cipro. Lo stallo politico si risolverà, comitati di saggi scriveranno il programma del governo prossimo venturo...Ci attendono le tradizionali "magnifiche sorti e progressive" . La ginestra, si sa è una pianta mediterranea... (dunque cresce anche a Cipro...). Siamo la terza economia dell'Eurozona, e non possiamo certo subire umiliazioni...Anche se...anche se...come osserva Alessandro Fugnoli nel suo commento settimanale ai mercati , in Europa il potere finanziario e monetario viene esercitato con regole che cambiano continuamente senza che mai nessuno ne discuta, se non una trentina di politici e i loro sherpa. Gli articoli 123 e 125 del trattato istitutivo della Bce, ad esempio, dopo essere stati citati per molti anni ogni dieci minuti (sono quelli che vietano il sostegno del debito dei singoli stati e le operazioni di monetizzazione) sono spariti d’incanto una mattina d’agosto senza un referendum o un dibattito parlamentare. Sono spariti nella testa della Merkel e sono di conseguenza usciti dalla scena del mondo. Esse est percipi, diceva Berkeley. Se smetto di pensare a una cosa e sono la Merkel, questa cosa cessa di esistere.

I

I Fuori dall'Europa i mercati si sono rassicurati: una soluzione a una crisi è meglio di nessuna soluzione, l'Europa è maestra nel kicking the can down the road e così l'SP500 ha raggiunto nuove vette storiche, superando quelle del 2007. Complice la debolezza dell'Euro (ma va...) ha guadagnato il 2,1% in una settimana, superato solo dall'indice immobiliare globale (+2,6%). Maglia nera per l'indice Eurostoxx (-1,7%).

Le migliori strategie questa settimane sono state la asset allocation passiva e la top2 con un progresso dello 0,9%, la peggiore la momentum and mean reversion che ha perso lo 0,8%.

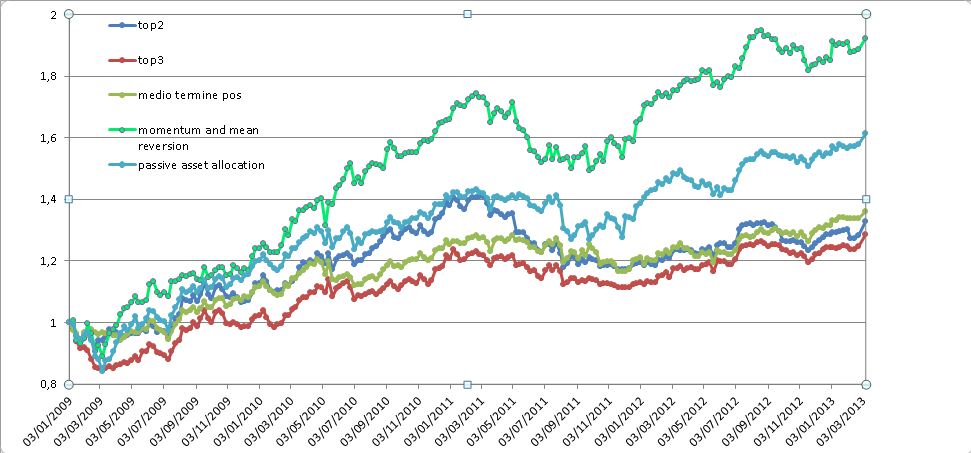

La tabella qui sotto riassume il profilo rischio/rendimento delle cinque strategie ( top2, top3, tendenza di medio periodo positiva, momentum and mean reversion e asset allocation passiva) negli ultimi 4 anni:

Nella figura è raffigurato l'andamento di un euro investito nelle cinque strategie dal 3 gennaio 2009 ad oggi.

E' bene ricordare che i rendimenti calcolati non tengono neppure conto dei costi di transazione e del prelievo fiscale. Mi preme comunque sottolineare che le analisi e le simulazioni descritte in questo blog sono da considerarsi sempre e comunque risultati teorici e relativi al passato. Chiunque decidesse di utilizzare le strategie descritte o qualsiasi altra informazione tratta da questo blog per decisioni di investimento se ne assume completamente la responsabilità.

C'è stato un po' di movimento nelle posizioni centrali e di coda della classifica settimanale: il cambio euro/dollaro occupa ora l'ultima posizione al posto delle materie prime, l'indice Eurostoxx la quarta posizione al posto dell'indice immobiliare globale. Le azioni europee hanno la tendenza di breve periodo negativa. I portafogli della strategie seguite hanno le composizioni seguenti (tutti i portafogli sono equipesati):

- top2: indice SP500 e obbligazioni trentennali dell'eurozona (invariato);

- top3: indice SP500, obbligazioni trentennali dell'eurozona e indice immobiliare globale (che prende il posto dell'indice Eurostoxx);

- tendenza di medio periodo positiva: indice immobiliare globale, indice Eurostoxx, indice Standard and Poor's 500 e obbligazioni trentennali dell'eurozona (invariato);

- momentum and mean reversion: obbligazioni trentennali dell'eurozona e materie prime (al posto del cambio euro-dollaro);

- strategia passiva: indice immobiliare globale, materie prime, indice Eurostoxx, indice Standard and Poor's 500 e obbligazioni trentennali dell'eurozona (invariato per costruzione).

In questo post ho descritto quali ETF negoziati a Milano replicano (in positivo o in negativo) gli indici che sono settimanalmente tracciati qui su Alfaobeta. Se volete fare delle analisi da soli, in questo post ho spiegato come procurarsi gratuitamente le serie storiche dei prezzi e dei NAV degli ETF mentre qui potete trovare qualche informazione sui costi di transazione nel mercato dei cambi.

Ecco l'aggiornamento al 29 marzo 2013